Saving RM10,000 in 12 months means RM833 per month, which is 32% of take-home. Tight but doable. Here is the exact system, not the inspirational version.

I am going to be honest with you from the start: saving RM10,000 in 12 months on a RM3,000 salary is possible, but it requires being deliberate about four or five specific decisions at once. It is not about cutting out your morning teh tarik.

The maths does not work on small sacrifices. It works on getting the big line items right and being systematic about the rest.

Here is the full breakdown, starting with what RM3,000 gross actually becomes in your hand.

Step 1: Know your real starting number

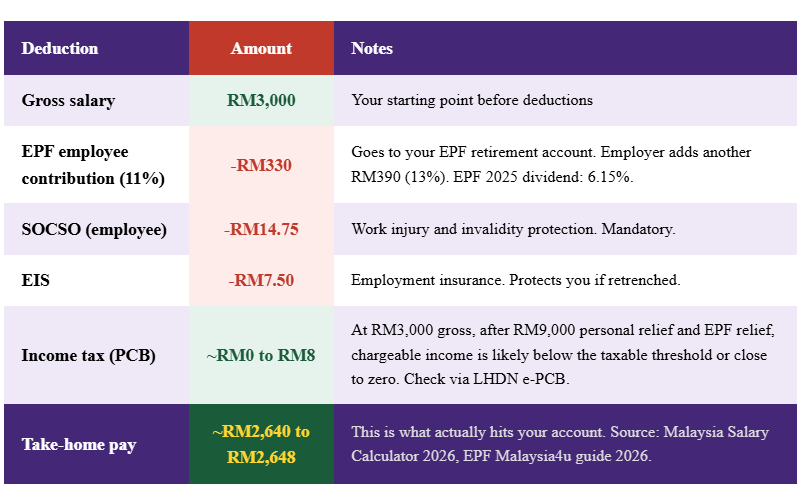

Most savings advice starts from the gross salary. That is not the number you work with. Here is what RM3,000 gross actually gives you in hand in Malaysia in 2026.

You are working with approximately RM2,640 per month. To save RM10,000 in 12 months, you need to set aside RM834 every month.

That is 31.6% of your take-home. Belanjawanku 2024/2025 estimates that a single adult in the Klang Valley who relies on public transport needs around RM1,970 a month for basic living expenses.

Subtract RM834 from RM2,640 and you have RM1,806 for living expenses.

That is below the Belanjawanku minimum, which means this goal requires making deliberate trade-offs and genuinely sticking to them.

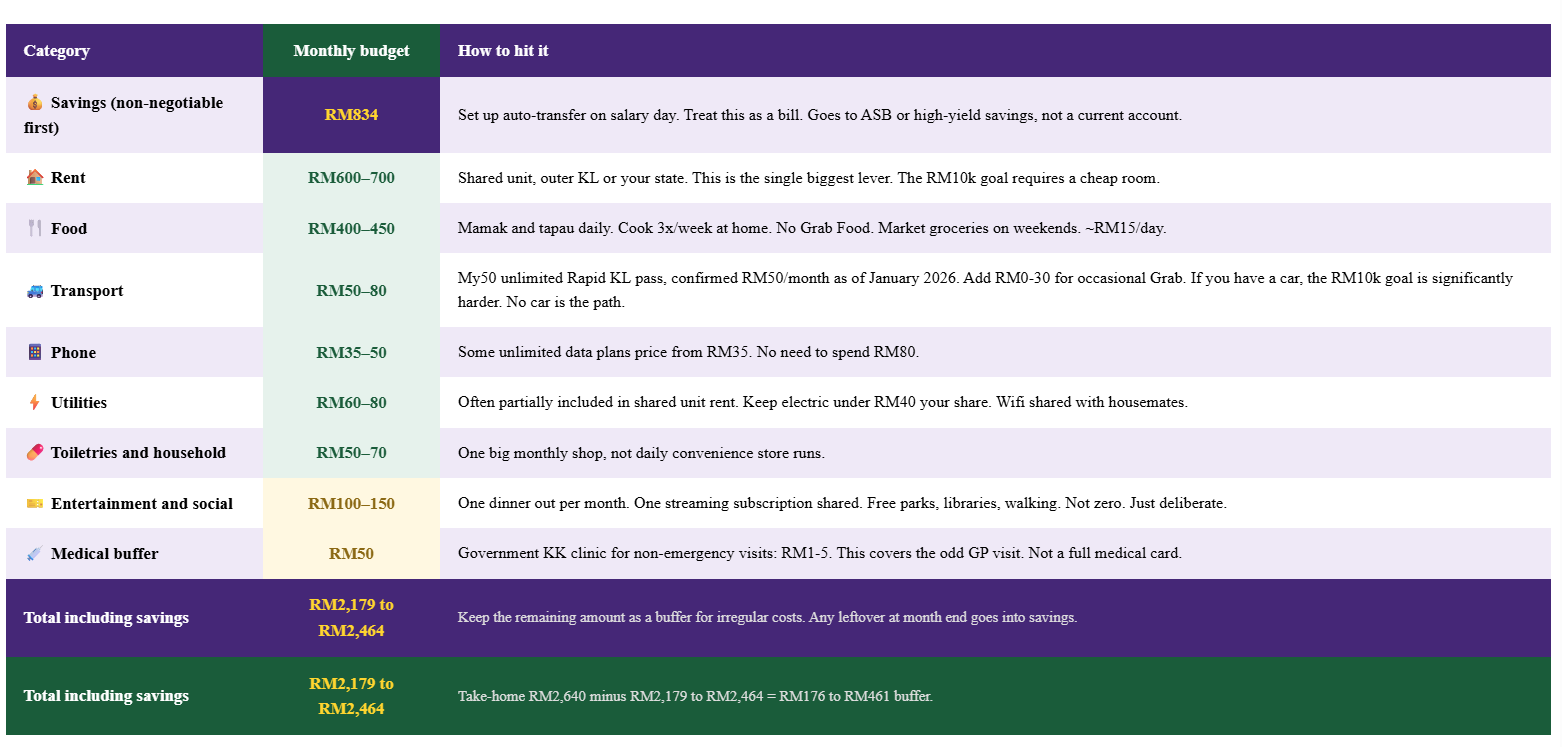

Step 2: The budget that actually makes RM10k possible

Here is the monthly budget breakdown that makes RM10,000 in 12 months work on RM2,640 take-home. Every number has a specific decision attached to it.

Step 3: The three decisions that actually determine whether you hit RM10k

The budget table above looks clean. Reality is messier. In my reading of Malaysian financial planning data, there are three specific decisions that determine whether someone on RM3,000 actually hits RM10,000 in 12 months or ends the year with RM3,000 to RM5,000 instead.

These three decisions account for more than 70% of the outcome.

Step 4: Where to put the money as it grows

Keeping RM10,000 in a current account earning 0% while you are trying to build it is a mistake. Here is where each phase of your savings should sit.

| Phase | Where to put it | Return | Why |

|---|---|---|---|

| RM0 to RM2,000 (months 1-3) | High-yield savings or tabung account (e.g. GXBank, Boost Bank, BigPay, etc.) | 2.5–3.5% p.a. | Liquid emergency access while building the base. Do not put early savings in ASB yet. |

| RM2,000 to RM10,000 (months 3-12) | ASB (Bumiputera) or EPF voluntary top-up Non-Bumi: high-yield savings or unit trust | 4.5–6.15% p.a. | ASB historically 4.5-6% p.a. over 10 years. EPF 2025 dividend 6.15%. Both beat fixed deposits significantly. |

| After RM10,000 is hit | Split: emergency fund (3 months expenses) stays liquid. Excess moves to longer-term investment. | Varies | Once RM10k is achieved, decide: is this your emergency fund or the start of an investment portfolio? |

The EPF angle you might be missing

At RM3,000 gross salary, the monthly EPF contribution comes up to RM720, made up of RM330 from the employee and RM390 from the employer. However, this amount does not go entirely into Akaun Persaraan, as new EPF contributions are split into 75% Akaun Persaraan, 15% Akaun Sejahtera and 10% Akaun Fleksibel. Over 12 months that is RM8,640 compounding at 6.15%. This is not accessible cash savings toward your RM10k goal, but it is real wealth building happening in parallel. Your voluntary top-up of the RM834 into EPF counts as additional savings and gives you EPF tax relief up to RM4,000 per year, reducing your taxable income. At RM3,000 gross this tax benefit is small, but every ringgit counts when the margin is this tight.

Step 5: The months that will try to break the plan

Every 12-month savings plan has at least two or three months that will try to derail it. On RM2,640 take-home with RM834 committed to savings, the buffer is thin.

Here are the known danger months and the pre-decided responses.

Raya / festive season (months with duit raya obligations)

Pre-decide a hard cap of RM100 to RM150 for raya spending including duit raya. Communicate this to family in advance if needed. Do not raid the savings account. Reduce that month’s food or entertainment budget instead. The savings transfer still goes out on salary day.

Unexpected medical expense

Government KK clinics charge RM1 to RM5 per visit. Use them. If a private GP is necessary, the RM50 monthly medical buffer covers one visit. For anything more serious, your SOCSO coverage applies for work-related incidents. Keep the first RM2,000 of savings liquid precisely for this. Do not deplete the full savings account.

A friend’s wedding / trip invitation

Pre-decide your social event budget for the year: RM300 total for weddings and group events. Attending a destination wedding on a RM3,000 salary while saving RM10k is not compatible with the goal. You can go to the dinner. You cannot go to Bali.

The month you skip the savings transfer

This will happen at some point. The plan is not ruined. Transfer whatever you can that month, even if it is RM200. Reset the full transfer the following month. One missed month costs you RM634 in lost savings but it does not cost you the goal if you continue. Stopping entirely after one bad month is what costs you the goal.

The 12-Month projection

| Month | Monthly saving | Cumulative total (approx at 3% p.a.) |

|---|---|---|

| 1 | RM834 | RM836 |

| 2 | RM834 | RM1,674 |

| 3 | RM834 | RM2,514 |

| 4 | RM834 | RM3,356 |

| 5 | RM834 | RM4,201 |

| 6 | RM834 | RM5,048 |

| 7 | RM834 | RM5,898 |

| 8 | RM834 | RM6,750 |

| 9 | RM834 | RM7,605 |

| 10 | RM834 | RM8,463 |

| 11 | RM834 | RM9,323 |

| 12 | RM834 | RM10,186 🎉 |