For many homeowners, finally paying off a housing loan is a huge milestone.

After years of monthly instalments, the bank finally issues the settlement letter, the commitment disappears, and it feels like the house is officially yours.

However, licensed financial planner Faiz Mohamad recently shared on Facebook that there is one important step many homeowners tend to overlook after settling their housing loan; removing the bank’s charge from the house grant.

In simple terms, even if the loan has been fully paid, the property may still be “tied” to the bank on paper if this process has not been completed.

Here are five things homeowners should know and do after paying off their housing loan.

1. Don’t assume everything is done once the loan is paid

Many people think that once the bank issues a settlement letter, the whole process is complete.

But according to Faiz, that is not always the case.

Even after the housing loan has been fully settled, the bank’s name may still remain on the house grant as the charge holder.

This means that from a documentation point of view, the property is still linked to the bank, even though the homeowner no longer owes the bank any money.

So while the monthly commitment may be gone, there is still an important legal and administrative step to complete.

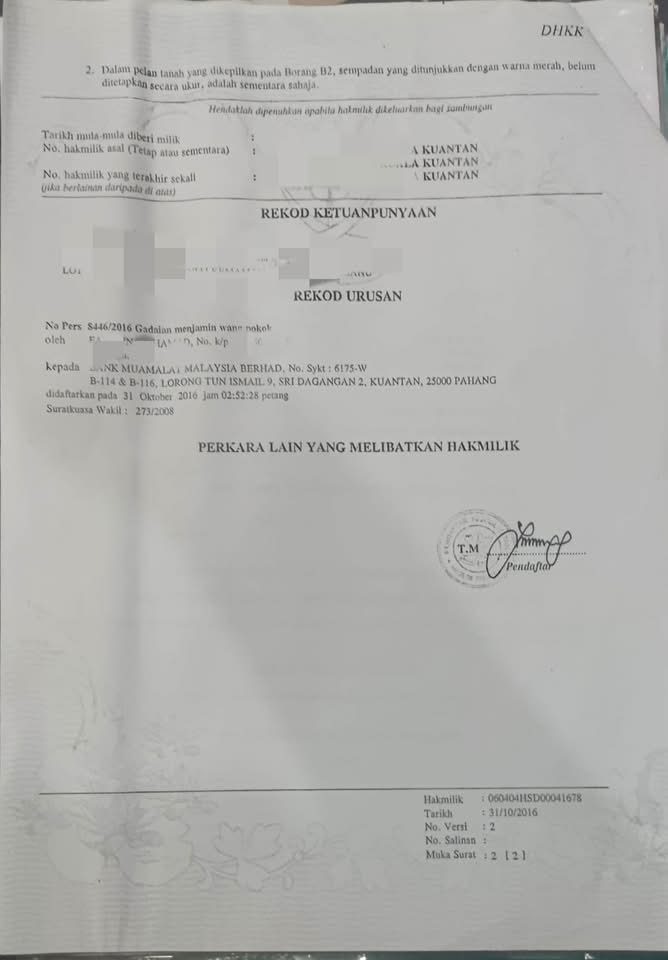

2. Remove the bank’s charge from the house grant

This process is known as Discharge of Charge, or pelepasan gadaian in Malay.

Faiz explained that the bank will issue the discharge documents after the housing loan has been fully settled.

After that, a lawyer will usually help register the discharge with the land office.

Once the process is completed, the bank’s name will be removed from the grant, and the property will be fully under the owner’s name without the bank’s restriction.

In other words, this is the step that makes the house “clean” on paper.

3. Do it early to make selling the house easier later

One reason this step is important is that it can make future property transactions smoother.

If the owner decides to sell the house in the future, having a clean grant can help speed up the process.

However, if the discharge has not been done, the homeowner may need to complete this step first before the sale can proceed smoothly.

This may cause delays, especially if documents need to be retrieved or if the bank has undergone changes over the years.

So instead of waiting until the house is about to be sold, Faiz advised homeowners to settle this matter early.

4. It can also make inheritance matters easier

Aside from selling the property, removing the bank’s charge can also help family members in the future.

Faiz pointed out that if the homeowner passes away, the heirs may find it easier to manage the property if the grant is already free from the bank’s name.

This is especially important when it comes to inheritance matters, as any additional paperwork or unresolved documentation may make the process longer and more complicated.

Having a clean grant may not solve every inheritance issue, but it can at least remove one possible obstacle for the family.

5. Don’t wait until documents go missing

Another reason homeowners should not delay the discharge process is the risk of losing important documents.

Faiz said some people keep their settlement letter for years without taking further action.

By the time they finally want to remove the charge from the grant, the documents may be hard to locate.

In some cases, banks may have merged, changed names, or closed certain branches, making the process of retrieving old records more troublesome.

This is why it is better to complete the process soon after the loan is fully paid, while the documents are still fresh and easily available.

Bonus: Review your cash flow after the loan is cleared

Besides removing the bank’s name from the grant, Faiz also reminded homeowners to review their monthly cash flow once the housing loan is fully paid.

This is because the money that used to go towards instalments is now “freed up”.

However, he warned that many people may end up spending the extra money on lifestyle upgrades without realising it.

For example, if someone had been paying RM1,500 a month for their housing loan over the years, redirecting that same amount into savings or investments could make a big difference over the next 10 to 20 years.

With compounding, the long-term effect can be significant.

Faiz said finishing a housing loan does not mean one’s financial journey is over.

Instead, it could be the beginning of a new phase, one where homeowners can focus on building real wealth.

The takeaway

Paying off a housing loan is definitely something worth celebrating.

But before homeowners consider the matter fully settled, it is important to check whether the bank’s charge has been removed from the house grant.

As Faiz put it, the house may already be paid for, but the grant should also reflect that clearly.

Only then can the homeowner truly say the property is fully theirs.