Buying your first home is exciting, but let’s be honest, the loan part can be seriously confusing.

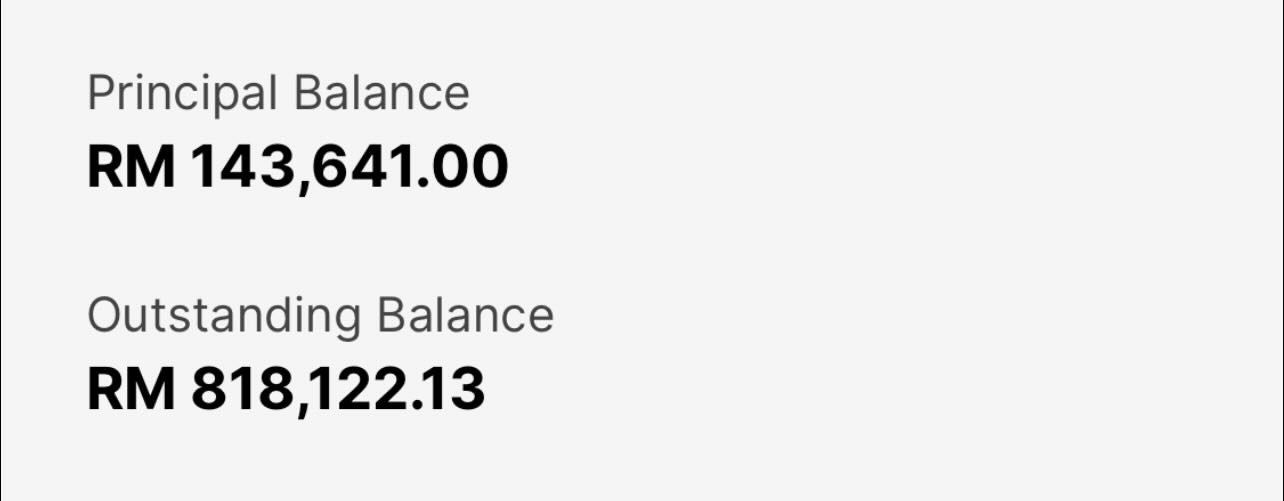

One Malaysian recently went viral after sharing that her house was priced at around RM218,000, but her banking app showed an outstanding balance of RM818,122.13.

Even more confusing, her principal balance was shown as RM143,641, while she was already paying around RM400 to RM500 a month for a house that was still under construction.

So, how does a RM218K house suddenly look like it has turned into RM818K debt?

Before anyone panics, here’s a simple breakdown of what may be happening.

1. Your bank may not release the full loan amount immediately

For houses that are still under construction, the bank usually does not pay the full property price to the developer at one go.

Instead, the money is released in stages, based on how much of the house has been completed.

For example, if your house costs RM218,000, the bank may not release the full RM218,000 immediately.

If the project is around 60% to 70% completed, the bank may have only released around RM143,000 to the developer so far.

That could explain why the principal balance in the screenshot showed RM143,641, even though the house price was said to be RM218,000.

In simple terms:

House price: RM218,000

Amount bank has released so far: RM143,641

Remaining amount: Will be released later as construction progresses

So the RM143K figure may not mean the house price changed. It may simply mean the bank has only paid part of the loan to the developer so far.

2. This is called progressive payment

The process where the bank releases money bit by bit is commonly known as progressive payment or progressive disbursement.

This usually happens for under-construction properties.

Think of it like paying a contractor to renovate a house.

You probably would not pay 100% before any work is done. Instead, you pay according to progress.

For example:

- When the foundation is completed, a portion is paid.

- When the structure is completed, another portion is paid.

- When the house is almost done, more money is released.

- When everything is completed, the final amount is released.

The same concept applies here.

The developer claims money from the bank according to the construction stage, and the bank releases the financing progressively.

3. Your RM400 to RM500 monthly payment may not be reducing the principal yet

This is the part many first-time homebuyers may not realise.

While the house is still under construction, the monthly amount you pay may only be progressive interest or progressive profit.

This means you are paying the bank for the amount it has already released to the developer.

For example:

- If the bank has released RM50,000, your payment is based on RM50,000.

- If the bank later releases RM100,000, your payment may increase.

- If the bank has released RM143,641, your payment may be based on that amount.

So when the buyer said she was paying around RM400 to RM500 a month, netizens explained that this amount may only be the interest or profit during the construction period.

That means it may not be reducing the actual principal balance yet.

Basically:

During construction: You may pay interest/profit only

After completion: You start paying the full monthly instalment

Only then: Your principal usually starts reducing properly

This is why some people feel like they have been paying every month, but the loan amount still does not seem to go down.

4. The monthly payment may increase once the house is completed

If you are currently paying RM400 to RM500 a month for an under-construction house, that may not be your final instalment.

Once the house is completed and the bank has released the full financing amount, your payment will likely change to the full monthly instalment stated in your agreement.

For example:

During construction, you may pay around RM400 to RM500 a month.

But after the house is completed, your full instalment could become around RM1,000 to RM1,300, depending on your financing amount, rate, and tenure.

So the smaller amount paid during construction is not the “real” full housing instalment yet.

It is more like a temporary payment while waiting for the house to be completed.

5. The RM818K outstanding balance may be linked to Islamic financing

Now, let’s talk about the scariest number in the screenshot: RM818,122.13.

Many netizens said this may be because the home financing is under Islamic financing.

In some Islamic financing structures, the amount shown may include the bank’s maximum selling price or maximum contracted amount over the full financing tenure.

This amount may be calculated using a ceiling profit rate.

In simple words, the bank shows the maximum possible amount under the contract, not necessarily the actual amount the buyer will end up paying.

Example:

House price: RM218,000

Financing tenure: 35 years

Ceiling profit rate: Higher maximum rate stated in the agreement

Outstanding amount shown: Could appear much higher because it includes the maximum contracted amount

That does not automatically mean the buyer must pay RM818K in real life.

It may be a maximum figure under the Islamic financing contract.

6. The actual payable amount may be lower because of ibra’ or rebate

In Islamic financing, there is something called ibra’, which means rebate.

This rebate can reduce the amount that the customer actually needs to pay, especially if the effective rate is lower than the ceiling rate or if the customer settles the financing early.

For example, the app may show a maximum outstanding amount of RM818K.

But if the buyer asks the bank, “How much do I need to pay if I want to settle today?”, the actual settlement amount may be much lower.

One netizen gave an example, saying that if the principal balance is around RM143,641 and the effective rate is around 4.4% over 35 years, the total payable would be nowhere near RM818K.

So the important thing is this:

Outstanding balance shown in app: May include maximum contract amount

Actual settlement amount: Must be checked directly with the bank

Rebate or ibra’: May reduce the final payable amount

This is why some netizens told the buyer not to panic just by looking at the app.

7. Extra payments may not automatically reduce your principal

Another useful reminder from netizens: if you want to pay extra to reduce your principal, do not simply transfer money and assume it will go straight to the principal.

Depending on the bank, extra payments may be treated differently.

Some banks may count it as advance payment for future instalments. Others may require you to specifically inform them that the extra payment is meant to reduce the principal or outstanding financing amount.

For example:

- Your monthly payment is RM500.

- You pay RM1,000 through online banking.

- You assume the extra RM500 reduces your principal.

But the bank may treat it as advance payment instead, unless you choose the correct option or notify them properly.

That is why some commenters advised buyers to walk in to the bank or contact customer service if they want to make principal payments.

The safest thing to ask the bank is:

I want to make an extra payment to reduce my principal. What is the correct way to do it?”

So, what should homebuyers ask their bank?

If you are also confused by your home financing statement, here are some questions worth asking:

- What is my actual principal balance?

- How much has the bank released to the developer so far?

- Is my current monthly payment only progressive interest or profit?

- When will my full instalment begin?

- Why is my outstanding balance higher than my house price?

- Does the amount shown include the Islamic financing ceiling rate?

- What is my actual settlement amount if I want to settle today?

- How does ibra’ or rebate apply to my financing?

- How do I make extra payments directly to principal?

The takeaway

A RM218K house showing an RM818K outstanding balance may look terrifying at first, but it does not always mean the buyer actually owes RM818K.

For under-construction homes, the bank may release money to the developer in stages. During that period, the buyer may only be paying progressive interest or profit.

And if the financing is under Islamic financing, the outstanding balance shown may include a maximum contract amount based on the ceiling profit rate, while the actual payable amount may be lower after rebate.

Still, every bank and financing agreement is different.

So, it is always best to check directly with the bank and ask for a clear breakdown of what each figure means.

View on Threads