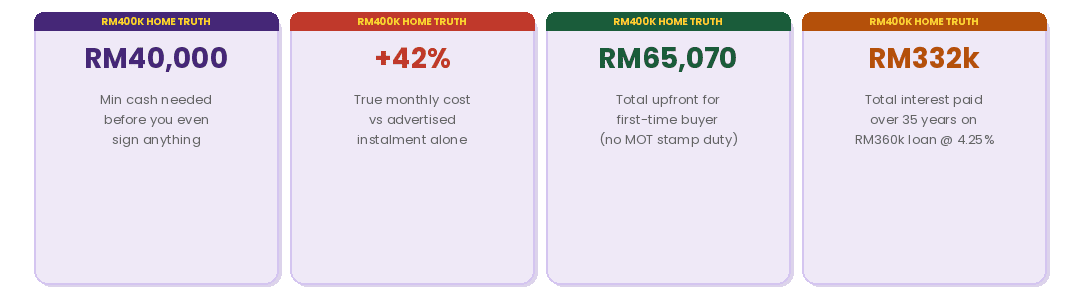

The bank quotes you RM1,648/month. Your actual monthly commitment is RM2,338. And before that first installment, you need RM65,000 cash sitting ready. Here is everything nobody puts in the brochure.

The property developer’s advertisement shows a bright kitchen, a happy couple, and a number: RM1,648 per month. That is what a RM400,000 home costs, apparently.

The installment is calculated correctly: RM360,000 loan at 4.25% over 35 years does produce a monthly repayment of RM1,648.

What the advertisement does not show is what you need in cash before you can even sign anything, every other cost that hits your bank account every single month after moving in, or the RM332,000 in interest you will pay over the life of the loan.

This article is the version of the property conversation that agents and developers do not volunteer.

Every number here is based on current Malaysian rates, gazette fees, and real 2025 market data.

None of it is designed to put you off buying property — property can be a sensible long-term financial decision for the right person at the right time. But it has to be a decision made with accurate numbers, not the one figure on a developer’s marketing banner.

Part 1: Before You Move In: The Upfront Cash You Actually Need

Most people know about the 10% down payment.

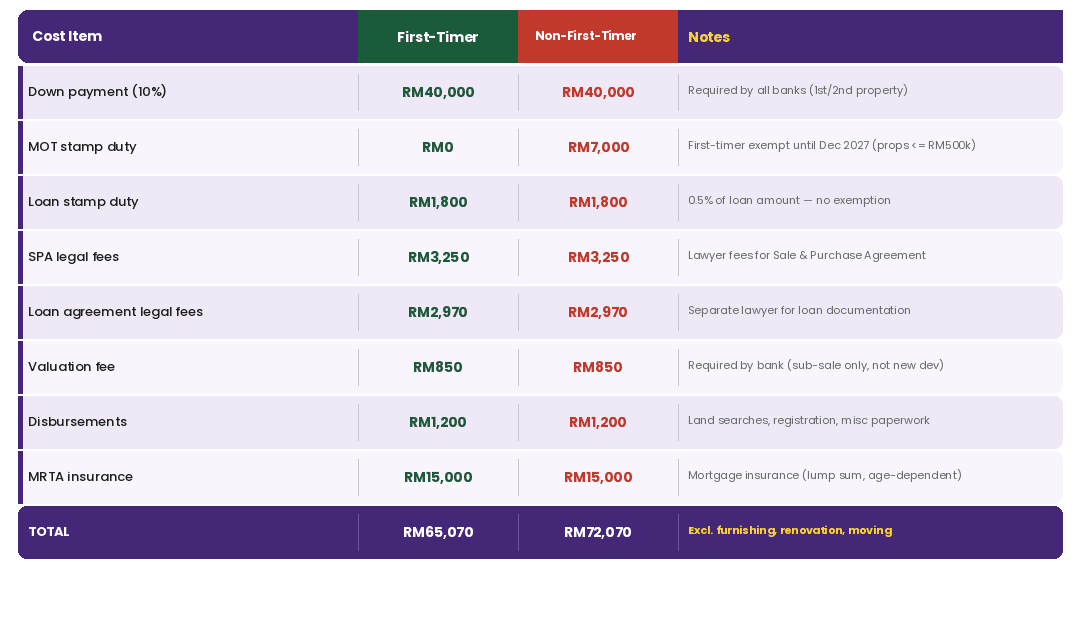

Not everyone realises that the down payment is just one of eight separate upfront costs that hit you before you ever receive the keys.

Here is the full picture for an RM400,000 property, assuming a 90% loan of RM360,000.

The down payment: RM40,000

For a first or second residential property below RM500,000, most Malaysian banks will lend up to 90%, meaning you pay 10% yourself.

On a RM400,000 property, that is RM40,000.

This money is not paid in one lump sum on one day.

Typically 2% to 3% is paid as an earnest deposit or booking fee when you agree to purchase, and the remaining 7% to 8% is paid when you sign the Sale and Purchase Agreement (SPA).

The bank only releases the loan once the SPA is signed and the legal documentation is progressing. Your RM40,000 needs to be liquid before you sign anything.

Stamp duty on the Memorandum of Transfer (MOT): RM0 or RM7,000

The Memorandum of Transfer is the document that transfers legal ownership of the property from the seller to you.

The stamp duty on this document is tiered:

1% on the first RM100,000, and 2% on the next RM400,000.

For a RM400,000 property, that works out to RM7,000.

However, first-time homebuyers purchasing properties priced at RM500,000 and below are fully exempt from this stamp duty under a scheme that has been extended until December 31, 2027.

If you have never owned a residential property in Malaysia before, this is RM7,000 you do not pay. If you have previously owned property, you pay the full amount.

Loan agreement stamp duty: RM1,800

Separate from the MOT stamp duty, the loan agreement itself is subject to stamp duty at 0.5% of the loan amount.

On a RM360,000 loan, that is RM1,800. There is no exemption for first-time buyers on this. It applies regardless.

The good news is that this is relatively straightforward and calculated automatically by your lawyer. Some developers also provide stamp duty subsidy to offset the expenses.

SPA legal fees: approximately RM3,250

You need a lawyer to prepare and execute the Sale and Purchase Agreement. Legal fees are set on a tiered scale: 1% on the first RM150,000 of the purchase price, and 0.7% on the next RM850,000. For a RM400,000 property: RM1,500 plus RM1,750 equals approximately RM3,250.

Some developers absorb SPA legal fees for new launches. Always check whether this applies and get it in writing.

Loan agreement legal fees: approximately RM2,970

Separate from the SPA lawyer, you (or the bank) appoint a lawyer to prepare the loan agreement documentation.

The fee is calculated on the same tiered scale applied to the loan amount: 1% on the first RM150,000 and 0.7% on the remainder. For a RM360,000 loan: RM1,500 plus RM1,470 equals approximately RM2,970.

In practice, the same law firm often handles both SPA and loan documentation, and the combined invoice may be slightly different from the sum of the two components.

Valuation fee: approximately RM850

If you are buying a sub-sale property (secondhand, not direct from developer), the bank will require an independent valuation before approving the loan.

The valuation fee is calculated as 0.25% on the first RM100,000 and 0.2% on the next RM1.9 million. For a RM400,000 property: RM250 plus RM600 equals RM850.

New launches from developers typically do not require a separate valuation, as the purchase price is the developer’s stated price.

Disbursements: approximately RM1,200

Disbursements are the miscellaneous administrative costs incurred by your lawyer on your behalf: land title searches, registration fees at the land office, bank processing charges, postage, and other sundry costs.

These are not separately published on a schedule but typically run to RM800 to RM1,500 for a standard residential transaction. Budget RM1,200 as a reasonable midpoint.

MRTA mortgage insurance: approximately RM15,000

Mortgage Reducing Term Assurance (MRTA) is a life insurance policy that pays off your outstanding home loan if you die or suffer total permanent disability during the loan tenure.

While it is not legally compulsory, most banks strongly encourage it and some make loan approval contingent on its purchase.

The cost is highly dependent on your age, the loan amount, and the coverage tenure. For a 30-year-old, RM360,000 loan, 35-year tenure, the MRTA premium is typically in the range of RM12,000 to RM18,000 paid as a lump sum.

RM15,000 is used here as a representative figure. The younger you are when you buy, the lower the premium. Delaying property purchase by even five years meaningfully increases this cost.

The upfront total — before you touch the keys

First-time buyer: RM40,000 + RM0 + RM1,800 + RM3,250 + RM2,970 + RM850 + RM1,200 + RM15,000 = RM65,070

Non-first-timer: Same as above but add RM7,000 MOT stamp duty = RM72,070

This is before furnishing, renovation, appliances, or moving costs — which for a basic setup easily add RM20,000 to RM50,000.

The EPF Account 2 option — check before you assume

First-time buyers are eligible to withdraw from EPF Account 2 to partially fund the down payment, legal fees, and stamp duty, but not the MRTA.

Log in to i-Akaun to check your Account 2 balance before assuming you need all RM65,070 in liquid savings.

Many Malaysians use this route to bridge the gap between their savings and the total upfront requirement.

Part 2: After You Move In – The True Monthly Cost

Now for the number that matters every single month for the next 35 years. The bank quotes RM1,648.

Here is what actually leaves your account every month when you own a RM400,000 strata property in the Klang Valley.

The loan installment: RM1,648/month

RM360,000 borrowed at 4.25% annual interest rate (current market rate based on OPR of 2.75% plus a typical bank spread of 1.5% for loans below RM400k), paid over 35 years.

It is also the only figure that appears in most property advertisements.

The 4.25% rate assumes a clean credit history and stable income — first-time buyers with strong CCRIS records and higher loan amount may get promotional rates as low as 3.55% from certain banks during campaign periods.

Maintenance fee and sinking fund: RM440/month

For a strata property: condominium, apartment, serviced residence, or gated community — you pay a monthly maintenance fee to the Joint Management Body or Management Corporation that runs the building.

This fee covers shared facility upkeep: lifts, lobby, guard house, swimming pool, gym, landscaping, common area electricity and cleaning.

For a mid-range development in the Klang Valley (Subang Jaya, Puchong, Cheras, Kepong), the rate typically runs RM0.30 to RM0.45 per square foot.

At RM0.40 per square foot for a 1,000 square foot unit, the maintenance fee is RM400 per month.

Under the Strata Management Act 2013, a separate sinking fund of at least 10% of the maintenance fee is also mandatory: an additional RM40 per month, reserved for major future repairs such as lift replacement, exterior repainting, or structural works.

Total: RM440 monthly.

This is not optional. Non-payment can result in legal action and a caveat on your title that blocks any future sale.

Assessment tax and quit rent: approximately RM75/month

Assessment tax (cukai taksiran or cukai pintu) is levied by your local authority: DBKL, MBPJ, MPKj, or equivalent, based on a percentage of the property’s estimated annual rental value.

For a RM400,000 condominium with an estimated rental value of around RM1,500 per month, assessment tax typically runs RM600 to RM900 per year.

Budget RM750 per year, or RM62 per month amortised.

Quit rent (cukai tanah) is a much smaller annual fee paid to the state government for the land. For strata properties, it is typically RM50 to RM200 per year.

At RM150 per year, that is RM12 per month. Combined: approximately RM75 per month. These are billed annually but must be budgeted monthly.

Fire insurance: approximately RM25/month

Fire insurance is required by most banks as a condition of the home loan.

It covers the structure of the building (not the contents) against fire and related perils. For a RM400,000 property, the annual premium is typically in the range of RM200 to RM400 depending on the insurer and the property’s construction type.

At RM300 per year, that is RM25 per month. This is separate from the MRTA (which covers the loan balance) and separate from home contents insurance (which covers your furniture, appliances, and personal belongings — worth considering separately).

Home repair and maintenance buffer: RM150/month

When you rent, you call the landlord. When you own, you are the landlord.

Air conditioning units need servicing (RM60 to RM150 per unit per service, twice a year).

Water heaters fail. Taps drip. Tiles crack. Paint peels.

Kitchen appliances die on weekends. None of this is covered by the building’s sinking fund, that is for common areas only.

Your own unit’s maintenance is entirely your responsibility. RM150 per month (RM1,800 per year) is a conservative buffer that covers routine servicing and minor repairs. In practice, the first few years after moving in tend to have higher costs as you discover issues the previous owner or developer did not disclose.

| Cost item | Monthly amount | Billed how |

|---|---|---|

| Loan installment | RM1,648 | Monthly, auto-debit |

| Maintenance fee | RM400 | Monthly, to JMB/MC |

| Sinking fund | RM40 | Monthly, to JMB/MC |

| Assessment tax (cukai taksiran) | ~RM62 | Annual (amortised) |

| Quit rent (cukai tanah) | ~RM12 | Annual (amortised) |

| Fire insurance | ~RM25 | Annual (amortised) |

| Home repair buffer | RM150 | Set aside monthly |

| TRUE TOTAL MONTHLY COST | RM2,338 | vs advertised RM1,648 |

Based on 1,000 sqft mid-range Klang Valley strata property. Maintenance fee at RM0.40/sqft. Loan at 4.25%, 35yr tenure. All figures approximate and vary by property and location.

The difference between RM1,648 and RM2,338 is RM690 per month — RM8,280 per year — that is not in any developer’s marketing material. Over 35 years, that gap represents RM289,800 of costs beyond the loan installment alone. This is why the question to ask is not “can I afford the installment?” but “can I afford the full monthly commitment of owning this property?”

Part 3: The Loan Interest Nobody Talks About

You borrow RM360,000. Over 35 years at 4.25%, you pay back RM692,336 in total.

The extra RM332,336 is pure interest. Money paid to the bank for the privilege of borrowing.

That is nearly the cost of the original property again, paid entirely in interest charges over time. This is not a criticism of home loan, interest is the cost of borrowing, and for most Malaysians a loan is the only way to access property ownership.

But it is a number that deserves to be front and centre in any honest property conversation.

The interest cost is most effectively reduced by making voluntary partial capital repayments when you can, any additional payment above the monthly installment reduces the outstanding principal, which reduces the interest charged in subsequent months.

Even an extra RM200 per month from year one can save tens of thousands of ringgit in total interest and shorten the loan tenure by several years. Check with your bank whether there is a penalty for early repayment before doing this. Most Malaysian home loans do not penalise partial repayments, but some do during the first few years.

What the salary requirement actually looks like

Banks use the Debt Service Ratio (DSR) to assess affordability, total monthly debt commitments divided by gross monthly income.

Most banks cap DSR at 60 to 70% for lower incomes and 70 to 80% for higher incomes.

But a healthier personal finance target is 50% or below.

At DSR 50%, you need a gross monthly salary of at least RM3,296 just to service the loan installment alone without any other existing debt.

To comfortably service the true monthly cost of RM2,338, you need approximately RM4,700 gross per month at DSR 50%.

If you have an existing car loan, personal loan, or PTPTN repayment, these reduce your available DSR headroom significantly.

Part 4: What First-Time Buyers Actually Get

Despite the heavy upfront costs, first-time buyers in Malaysia have access to meaningful support that can significantly reduce the cash required to get started. These are worth understanding in detail before concluding that homeownership is impossible.

MOT stamp duty exemption — saves RM7,000 -> Until Dec 2027

Full stamp duty exemption on the Memorandum of Transfer for first-time buyers purchasing properties at RM500,000 and below.

This is the single largest cost reduction available and saves RM7,000 on a RM400,000 purchase.

Confirm your eligibility with your lawyer: you must declare you have not previously owned residential property in Malaysia.

EPF Account 2 withdrawal — reduces cash needed -> Check i-Akaun now

EPF members can withdraw from Account 2 for the down payment, legal fees, and stamp duty (not MRTA).

If your Account 2 has RM20,000 to RM30,000, this meaningfully reduces the liquid cash requirement.

The withdrawal must be applied for separately from the loan process — factor in three to six weeks of processing time before the money hits your bank.

Government-assisted loan schemes — SJKP, PR1MA -> Income ceiling applies

For buyers who cannot qualify for commercial bank loans due to income or DSR constraints, government-backed schemes like Skim Jaminan Kredit Perumahan (SJKP) and PR1MA’s housing programmes provide alternatives with different eligibility criteria.

These schemes typically have income ceilings and property price caps, but can be the difference between accessing homeownership and not. Check the latest eligibility requirements directly with the respective agencies as they are updated regularly.