Having a side income sounds like a smart move, especially when many Malaysians are taking up part-time work to earn extra money.

Some become Takaful agents, property agents, unit trust consultants, or sell products such as Coway, Cuckoo, and others.

But according to one Malaysian man, there is one important thing people should not overlook: declare your side income, even if the amount seems small.

In a Threads post, user Saipul Nizam shared his personal experience after he was allegedly penalised for not declaring his part-time Takaful income in previous tax filings.

He said the whole incident became a lesson for him, and he hoped others would not repeat the same mistake.

1. Don’t assume small side income does not need to be declared

According to Saipul, he had been working a salaried job since 2005 and had never missed his yearly e-Filing.

For years, he said he declared his employment income properly and had no issues with his tax filing.

However, things changed after he started doing part-time Takaful work in June 2016.

At the time, Saipul had two income sources, which were his salary and his part-time Takaful income. However, he admitted that he only declared his salary because he thought the side income was not big enough to be included.

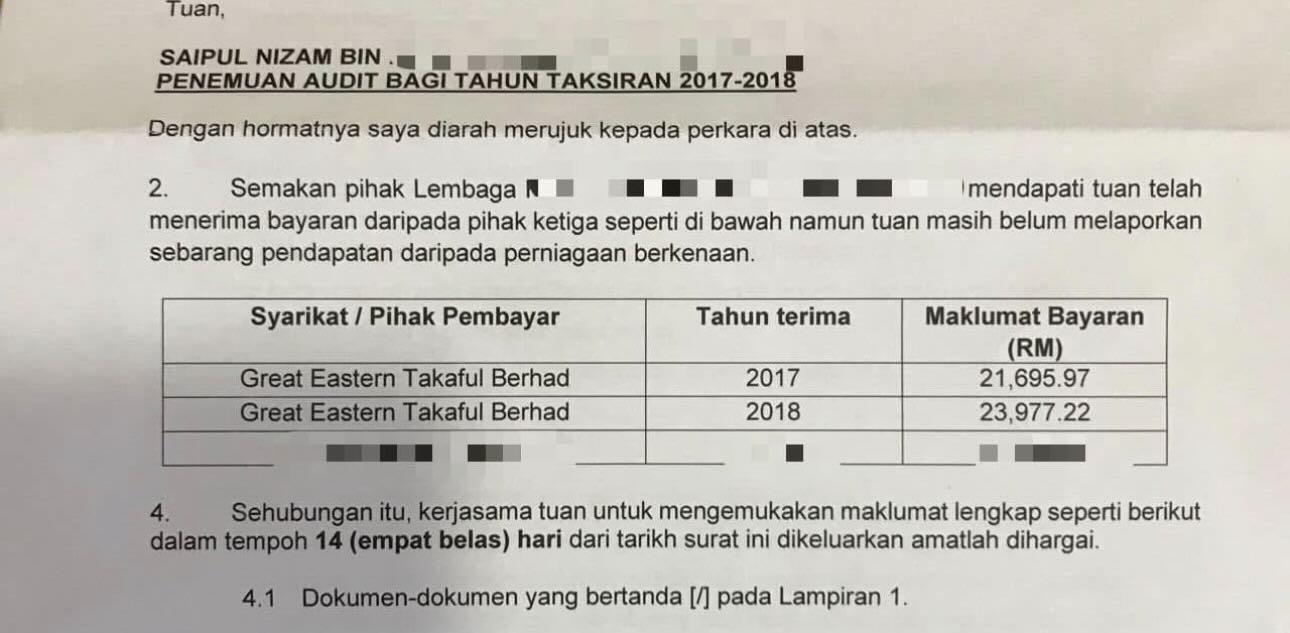

He claimed his part-time Takaful income was around RM5,000 in 2016, RM21,000 in 2017, and RM23,000 in 2018.

“My mistake back then was thinking that if the income was small, I didn’t need to declare it. Turns out, I was wrong,” he wrote.

2. Once you declare a new income source, old records may be checked too

Saipul said the issue only surfaced when he filed his tax for 2019.

That year, he had left his full-time job in July, which meant his salary income became lower than in previous years. At the same time, his Takaful income had increased to around RM50,000 a year.

Because of that, he declared two sources of income for 2019, namely RM36,000 from salary and RM50,000 from Takaful business income.

According to Saipul, the change triggered the system and he later received a letter asking him to attend an audit and bring supporting documents.

He said he was not too worried about the 2019 audit because he had declared the income and kept his documents properly. The audit for that year went smoothly.

However, the matter did not end there.

Three months later, Saipul claimed he received another letter. This time, he said his previous Takaful records were checked, and it was found that he had not declared the income from 2016 to 2018.

3. Commission income may already be recorded by the company

One major reminder Saipul shared is that commission-based income can still be traceable, even if a person does not declare it during e-Filing.

According to him, companies such as Takaful providers may still issue related income records.

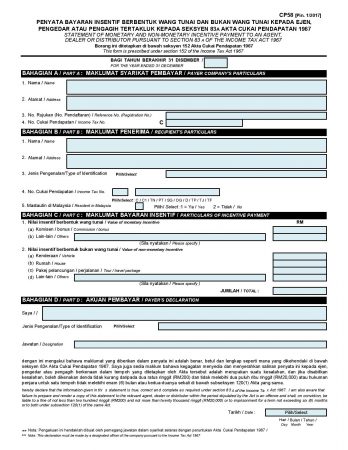

A commenter also pointed out that commission from Takaful, Amway, property, Coway, Cuckoo, unit trust, and similar sources are usually reported by the company through CP58.

Saipul agreed, saying companies would submit records on their side, and taxpayers should declare their income based on those records.

According to LHDN, Form CP58 is a statement of monetary and non-monetary incentive payments to an agent, dealer, or distributor. LHDN also states that employers are required to prepare and provide CP58 to each agent, dealer, or distributor by 31 March of the following year.

In other words, even if the amount feels “small”, there may already be an official record of it.

“Whether the income is a lot or just a little, just declare it,” Saipul wrote in a comment.

4. Keep receipts and supporting documents properly

Saipul claimed that he was initially told the penalty amount was around RM15,000 for the years 2017 and 2018.

However, he explained that the amount was not final as the calculation would depend on his net income after expenses, not simply the full amount received.

As a Takaful agent, he said the income was not 100 per cent profit because there were also expenses such as training, gifts, client-related items, and other business costs.

Because of that, he had to prepare a Profit and Loss summary to show his income and expenses.

After submitting the adjustment based on the documents he still had, Saipul claimed the penalty was reduced from RM15,000 to around RM6,000. In one comment, he also said it was later reduced to about RM5,000.

However, he admitted that it could have been reduced further if he had more supporting documents and receipts from those years.

LHDN also reminds taxpayers to keep records and relevant documents for seven years for audit purposes.

5. Prepare a Profit and Loss summary if you earn business income

For those doing side jobs or commission-based work, Saipul said it is useful to prepare a Profit and Loss summary.

This is because not all money received is considered pure profit, especially if there are business-related expenses involved.

When one commenter asked how to start declaring Takaful income after previously working as an employee, Saipul advised that employment income is usually filed under Form BE, while Takaful income should be filed under Form B as business income.

He also said he would usually prepare a Profit and Loss summary based on CP58 before keying in the details during e-Filing.

According to LHDN’s FAQ, commission income is treated as business income and should be reported in Form B.

6. Don’t wait until audit time to organise your records

For Saipul, one of the hardest parts was not just the penalty, but trying to find old receipts and documents from several years ago.

He said the receipts from 2017 and 2018 were already difficult to trace because they were from three to four years earlier.

That is why he advised others to start organising their documents early instead of waiting until they receive an audit letter.

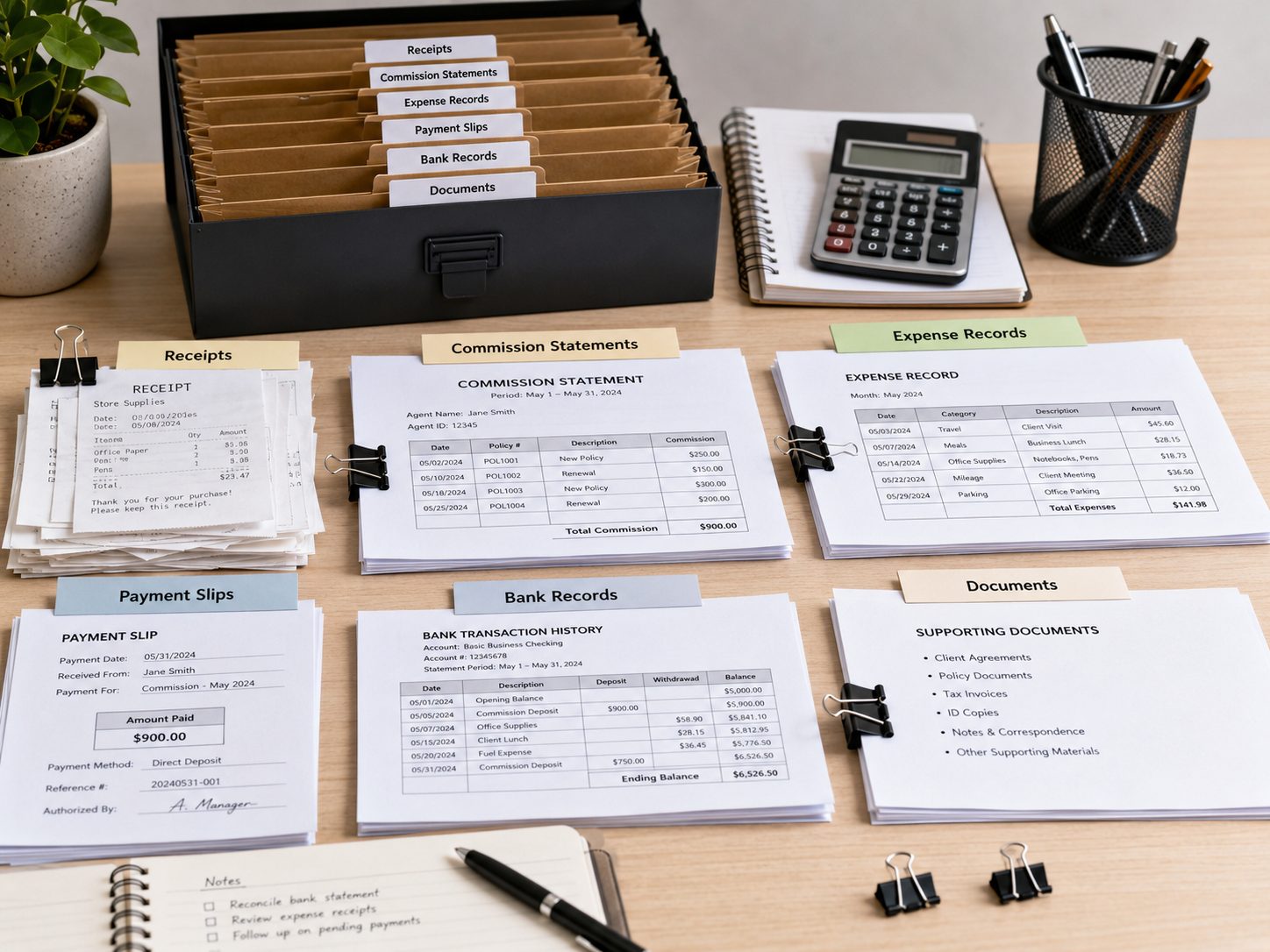

This includes keeping receipts, commission statements, expense records, payment slips, bank records, and any documents that can support the income or deductions declared.

7. Declare it even if it is only RM2,000 to RM3,000 a year

Saipul ended his post by reminding Malaysians not to underestimate small side income.

He said whether the income comes from selling Coway, Cuckoo, property, unit trust, Takaful, or other part-time work, it is better to declare it.

He added that his wife also does part-time Cuckoo work and earns around RM2,000 to RM3,000 a year, but he still asks her to declare it so she will not face the same issue.

‘ I didn’t expect LHDN to cross-check when my part-time record actually started’

Speaking to WeirdKaya, Saipul shared that he had actually expected LHDN to audit his 2019 filing after he started declaring his Takaful income.

He explained that he had been doing part-time Takaful since 2016, but only started declaring it in 2019 after he left his engineering job midway through the year.

According to him, if he had only declared his engineering income for 2019, it would likely have triggered questions from LHDN as he only worked until July that year.

“So when I declared both my engineering income and Takaful income in 2019, I already expected LHDN to audit me,” he told WeirdKaya.

Saipul said he had prepared all the necessary documents, and the 2019 audit went smoothly without any issues.

“I thought everything was settled. But I didn’t expect LHDN to cross-check when my part-time record actually started,” he said.

That was how the issue of undeclared income from 2017 and 2018 surfaced. Saipul added that LHDN also found his 2016 income, but no penalty was imposed for that year as the amount was very small.

His advice to those with side income

Saipul said his biggest advice to those doing any form of side income is to declare it, no matter what type of part-time work it is.

He said people should not worry too much, as declaring income does not automatically mean they will have to pay tax.

“If your salary and part-time income are below RM34,000, you usually won’t have to pay tax. We declare because we don’t want issues later,” he said.

He also said many people may not intentionally avoid declaring their side income, but simply do not realise that companies may issue CP58 records to LHDN.

According to Saipul, once a company issues CP58, LHDN can see details of the income from the very first day the person started doing part-time work.

“When you don’t declare it, it’s only a matter of time before it gets detected. Sooner or later,” he said.

What documents helped him during the process

Saipul said that for those with business income, preparing a Profit and Loss summary is important.

He shared that he kept receipts, invoices, credit card statements, and other supporting documents. For expenses such as petrol, toll and parking, he often used his credit card, which later helped him retrieve old statements.

He said that if he bought gifts for clients through platforms such as Shopee, he would print and keep the invoice as proof.

According to him, during an audit, the officer would usually look at the Profit and Loss summary first, while receipts and other documents should be kept on standby in case they are requested.

He also shared a practical tip for keeping receipts.

I paste the receipts on white paper and print them again because the carbon on receipts fades easily,” he said, adding that taking photos of receipts and saving them digitally can also work.

How the penalty was reduced

Saipul said the main thing that helped reduce his penalty was the Profit and Loss summary he prepared.

Although the transactions were already three years old by then, he was still able to retrieve many of his credit card statements by contacting the bank.

Because of that, he could still show several business-related costs and deduct them as expenses.

However, he said some expenses could no longer be claimed because he did not keep the receipts.

“For food and toll costs, I could no longer declare them because I didn’t keep the receipts,” he explained.

Following the incident, Saipul said he now declares everything, including his general insurance income of around RM1,000 a year, which he includes in his Profit and Loss summary.

He also said his wife, who works as a lecturer and does Cuckoo part-time, now declares her side income as well, even though the amount is not high.

“Her Cuckoo income is not much, but I still ask her to declare it, prepare a P&L summary, and include the Cuckoo income too,” he said.

The lesson here is simple

The main takeaway from Saipul’s experience is straightforward: if you earn extra income, do not assume it is too small to declare.

Even if no tax is eventually payable, declaring it properly and keeping the right documents can save you from bigger problems later.

For those unsure about how to declare part-time or commission-based income, it is best to check LHDN’s guidelines or speak to a licensed tax agent.

View on Threads