You’re at a traffic light. Some guy rear-ends you. It is not your fault. There’s dashcam footage, witnesses, the whole thing. But then you panic, call your insurer, say “I got into an accident,” and claim through your own policy without knowing the correct process.

Six years of No Claim Discount, gone.

Your next renewal premium goes up by hundreds of ringgit. And all of that is completely, totally, avoidably preventable.

This is the guide to what you actually do when someone else hits your car in Malaysia from the moment of impact to collecting your car from the workshop, so you protect your NCD, claim the right way, and don’t fall for the scams that happen at accident scenes.

First: What is NCD & why does it matter so much?

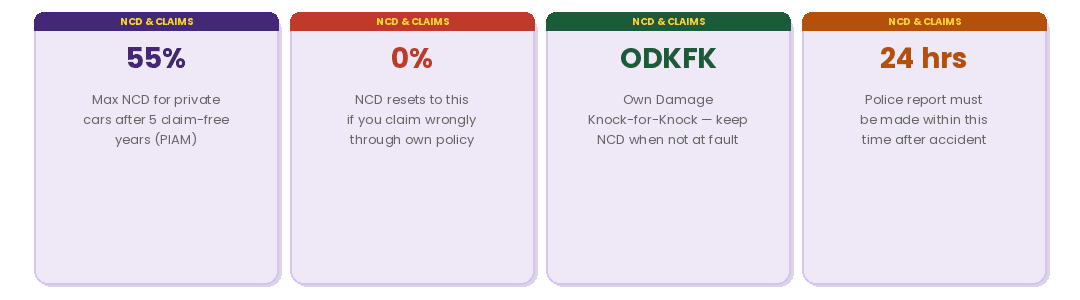

NCD (No Claim Discount) is a discount on your basic motor insurance premium that grows every year you go without making a claim.

It is set by PIAM (Persatuan Insurans Am Malaysia) and applies uniformly across all Malaysian insurers: no negotiation, no variation.

Here’s how it compounds over time for a private car:

Let that RM1,100/year saving sink in. If your base premium is RM2,000 and you’ve reached 55% NCD, you are paying RM900, just under half price.

Every single year.

Permanently, as long as you don’t claim. That is why losing your NCD to someone else’s accident is such a significant financial hit — and why knowing exactly how to protect it matters so much.

You can check your current NCD at mycarinfo.com.my/ncdcheck/online using your car plate and IC number — it’s free and takes about 30 seconds. Check it now if you don’t know what yours is.

Key fact about NCD

Your NCD is tied to you as the owner, not the car or the insurer.

If you sell your car, you can transfer the NCD to your new car (or withdraw it and use it within 12 months).

NCD does not transfer to another person and only between vehicles registered under your own name.

Step 1: What to do at the scene — the first 30 minutes

What you do in the 30 minutes after impact determines whether your claim is clean or complicated. Here’s the full breakdown:

Step 2: File a Police Report Within 24 Hours

Filing a police report within 24 hours is a legal requirement in Malaysia. It is also the foundation of your entire insurance claim.

Without a police report, there is no claim.

Without a police investigation outcome (the result of the investigation, which confirms who is at fault), there is no ODKFK.

These are two different documents: the report confirms the accident happened, the investigation outcome determines fault.

What to bring to the police station:

- Your IC and driving licence.

- Your car’s grant (geran/registration card).

- Your insurance policy details.

- All photos from the accident scene.

- The other party’s details you collected.

- Your dashcam footage (a copy).

- A simple sketch of the accident from memory (the officer will ask for this).

Request a certified copy of the police report (Laporan Polis) before you leave the station — you will need this for your insurance claim.

The investigation result (keputusan siasatan) will come separately, usually after the police complete their investigation.

Some cases are resolved quickly; others take weeks. Your claim can proceed using the police report while the investigation result is pending, but ODKFK requires the investigation outcome confirming the other party’s fault.

Step 3: Notify Your Insurer Within 7 Days

Regardless of which claim route you choose, you must notify your insurer within 7 days of the accident. This is a standard requirement across all Malaysian motor insurers. Failing to notify in time can complicate or invalidate your claim. Call their 24-hour hotline or submit through their app — most major insurers in Malaysia now offer app-based claim notification.

When you call, be factual: describe what happened, confirm you were not at fault, and ask specifically about your ODKFK (Own Damage Knock-for-Knock) options. Tell them you have police report documentation and dashcam footage. Do not accept their first suggestion without understanding what it means for your NCD.

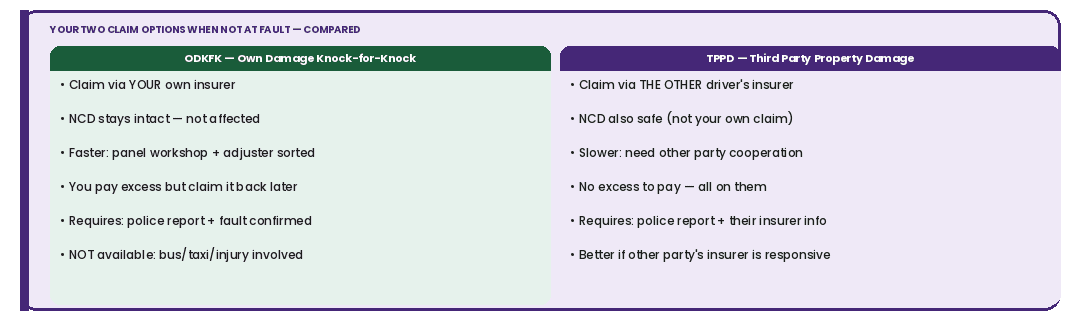

Step 4: Choose Your Claim Route — ODKFK or TPPD?

This is the most important decision in the entire claims process. When you’re not at fault in a car-to-car accident, you have two claim routes.

Both protect your NCD, but they work differently and suit different situations.

Option A: ODKFK — Own Damage Knock-for-Knock

This is Bank Negara Malaysia’s preferred route, clarified in updated guidance in 2025. You claim through your own insurer.

Your NCD is fully protected because the claim is categorised as not-your-fault.

BNM has also cut processing times significantly: own damage claims are now processed 20 working days faster on average.

ODKFK is available only when: The accident is confirmed car-to-car (not involving motorcycles). The police investigation outcome confirms the other party is at fault. The other vehicle is insured by a Malaysian-licensed insurer.

Also,there are no bodily injuries or fatalities involved. The other vehicle is not a commercial vehicle — no taxis, buses, Grab cars, school buses, or e-hailing vehicles.

Option B: TPPD — Third Party Property Damage Claim

You claim directly against the other driver’s insurer. This also preserves your NCD (since you’re not claiming through your own policy).

However, it is slower: you need to interact directly with a third party’s insurer who may be less cooperative, and you will likely need to pay for repairs upfront before seeking reimbursement.

This route is useful if the other party’s insurer is highly responsive, or if ODKFK is not available (e.g. motorcycle involved).

What about CART — Compensation for Assessed Repair Time?

If you are not at fault, you can also claim CART from the other party’s insurer. This is compensation for the days your car is in the workshop being repaired. It is calculated by the loss adjuster based on the repair complexity, not how long the workshop actually takes.

For private cars, CART rates range from RM30 to RM50 per day based on engine capacity.

Step 5: Send to Panel Workshop Only

Your car must go to an approved panel workshop for your claim to be processed cleanly. Sending it to any random workshop, even a good one, can result in your insurer rejecting or reducing the claim, or requiring you to pay out of pocket first and seek reimbursement.

Your insurer’s website will list all panel workshops.

Most major insurers also have apps or hotlines where they can arrange a tow to the nearest panel workshop directly from the accident scene.

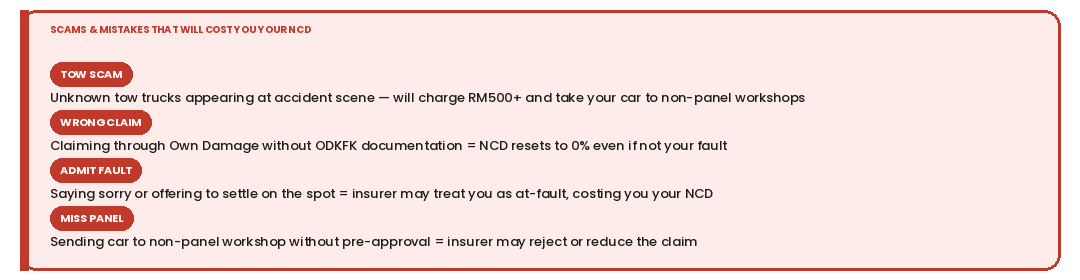

Also note that unofficial tow trucks appear at accident scenes within minutes, sometimes before the police arrive.

They will offer to take your car to a “partner workshop” where they get kickbacks.

The consequences are: inflated repair bills (which inflate your insurer’s costs and raise your next year’s premium), repairs done at non-panel workshops (which your insurer may not cover), and potential claim rejection.

Only accept towing from your insurer’s appointed operator.

Call your insurer’s hotline immediately after the accident and let them arrange it.

Step 6: Submit Documents and Track Your Claim

For an ODKFK or Own Damage claim through your own insurer, you will need to submit: your completed claim form, a copy of your IC and driving licence, your vehicle registration card (geran), the certified police report copy, photos of the damage, your dashcam footage (if available), and the other party’s vehicle details and insurance information.

The panel workshop will help coordinate the loss adjuster inspection: you don’t need to arrange this separately.

BNM’s 2025 reforms also mandate that insurers keep you updated at every stage of your claim. You should not be left waiting without communication.

If your insurer goes silent for more than a few working days without an update, follow up proactively. Most insurers now have claims tracking through their app or online portal.

When Your NCD Will STILL Be Affected (Know These Exceptions)

Should you ever pay out of pocket instead of claiming?

If you are at fault and the damage is minor: a small dent, a scratch, a cracked light, run the numbers before claiming.

The calculation is simple: compare the repair cost versus the cost of losing your NCD for the next renewal period (and the years to rebuild it).

General rule of thumb: if the repair cost is less than your annual NCD saving, you can opt to pay it by youself. If it’s significantly higher (e.g. major body damage, airbag deployment, structural damage), claim that’s what insurance is for.