I remember when I bought my car. The salesperson showed me the monthly instalment figure. I did the simple maths: instalment times number of months, and thought I understood what the loan was costing me. I did not.

What I did not know was that the way interest was being calculated meant that if I ever tried to settle the loan early, I would save far less than I expected.

The system was neither transparent nor designed in my favour.

That changes from 1 June 2026.

The Hire Purchase (Amendment) Act 2026 was gazetted on 30 January 2026 and takes effect on 1 June 2026, with a transition period for lenders to update their systems until 31 March 2027.

It abolishes two mechanisms that have quietly disadvantaged Malaysian car loan borrowers for decades.

These were the flat rate and the Rule of 78.

They are now replaced by the Effective Interest Rate (EIR) and the reducing-balance method.

If you have a car loan, or are planning to take one, you need to understand what just changed.

The Old System: What Flat Rate and Rule of 78 Actually Meant

Under the old system, when your bank told you the interest rate on your car loan was “3%,” that was a flat rate.

It was calculated on the original loan amount for the entire loan period, regardless of how much you had already paid back.

For example, if you borrowed RM60,000 over 9 years, interest was charged on RM60,000 all the way through, even in year 8 when you only owed RM5,000.

The Rule of 78 made this worse.

The name comes from the sum of the digits 1 through 12, which equals 78, used as the denominator when allocating how much of each instalment goes to interest.

The result was that a disproportionately large share of interest was paid in the early months of the loan.

In Month 1, out of a RM1,060 payment on a RM12,000 loan, RM110.77 went to interest and only RM949.23 reduced your actual debt.

By Month 12, only RM9.23 went to interest.

Most of what you owe the bank in interest was paid in the first third of your loan.

And if you tried to settle early? You had already paid most of the interest, but still owed most of the principal. You were penalised for being financially responsible.

What “3% flat rate” actually costs you

An analysis by The Edge Malaysia found that borrowers paying a stated 3% flat rate under the Rule of 78 were actually paying an Effective Interest Rate of 5.5%.

The stated rate and the true cost of borrowing were completely different numbers but banks were not required to show you the real one.

From 1 June 2026, they must.

The New System: EIR and Reducing Balance

From 1 June 2026, all new hire purchase agreements must use the Effective Interest Rate (EIR) and the reducing balance method.

Here is what that means in plain terms.

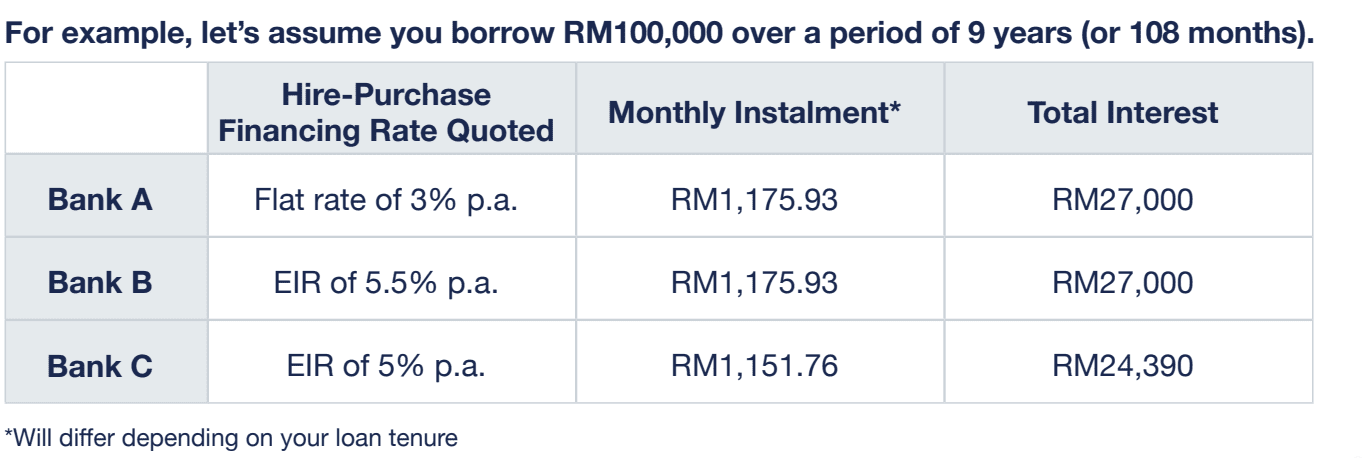

The above example illustrates that your monthly instalment remains the same with both Bank A and Bank B, where you end up paying a monthly instalment of RM1,175.93 and the same total interest of RM27,000.

With Bank C, you end up paying a lower monthly instalment of RM1,151.76 and a lower total interest of RM24,390. For a loan with a 9-year tenure, an EIR of 5.5% p.a. is equivalent to a flat rate of 3% p.a.

Hence, even though the flat rate may appear cheaper at first glance, it does not reflect the true cost of financing costs borne by you. It actually makes the hire-purchase product seem cheaper than it really is.

Reducing balance: interest on what you actually owe

Under the reducing balance method, interest is calculated every month on your outstanding loan balance on the outstanding balance, not the original amount.

Month 1 on a RM60,000 loan: interest on RM60,000.

By month 24 when you have paid down to RM42,000: interest only on RM42,000.

As you pay down your debt, your interest charge falls proportionally. This is how home loans have always worked. Car loans are now joining them.

EIR: the rate that tells you the truth

The Effective Interest Rate must now be displayed in all marketing materials and loan agreements.

It reflects the true cost of borrowing and what you are actually paying annually relative to what you still owe.

This makes it possible, for the first time, to do an apples-to-apples comparison of loan offers from different banks.

Previously, comparing a 2.8% flat rate from one bank to a 3.1% flat rate from another told you very little about which was actually cheaper in real terms.

Under EIR disclosure, the comparison becomes meaningful.

The EIR is capped at 17% per annum for loans of up to five years, and 16% per annum for loans of more than five years.

Early settlement: finally worth doing

This is the change with the most immediate financial impact for many Malaysians.

Under the old Rule of 78 system, settling a car loan early saved very little, because most of the interest had already been paid in the front-loaded schedule.

If you settle midway, you can save about 50% of the total interest. Under the old system, the saving was maybe only 5% or 10%.

That is a transformational difference for anyone considering early loan settlement.

| Feature | Old system (before June 2026) | New system (from June 2026) |

|---|---|---|

| Interest calculation | Flat rate on original loan amount | Reducing balance on outstanding amount |

| Interest allocation | Front-loaded via Rule of 78 | Even spread as balance reduces |

| Rate disclosed | Flat rate only (misleading) | EIR must be displayed — the true rate |

| Early settlement saving | ~5% to 10% of remaining interest | ~50% of remaining interest |

| Total interest paid (full tenure) | Same | Same |

| Digital signatures | Physical signatures only | Electronic/digital signatures permitted |

Sources: Hire Purchase (Amendment) Act 2026, BNM media workshop (PaulTan.org, Nov 2025), The Edge Malaysia analysis, RinggitPlus car loan guide (Apr 2026)

What About Existing Loans? The Goodwill Discount

If you already have a car loan signed before 1 June 2026, it does not automatically convert to the new system.

But the banking industry has announced a “goodwill discount” initiative for existing fixed-rate hire purchase agreements settled early after the Act takes effect.

This is a voluntary early settlement rebate that banks will offer on outstanding interest for loans signed before the new law.

It gives existing borrowers a more meaningful rebate than the Rule of 78 previously allowed.

The goodwill discount applies to individuals and micro and small businesses with existing fixed-rate hire purchase agreements, provided the account is not significantly overdue or under legal action.

If you have been considering settling your car loan early — to sell the car, upgrade, or simply clear the debt — the period from June 2026 onward may be more financially rewarding than before.

Contact your bank to get the settlement amount under the goodwill discount and compare it to what you would have paid under the old calculation.

There is also a provision for existing borrowers who wish to mutually agree with their lender to convert to the new reducing balance method.

This is not automatic and requires agreement from both parties — but it is an option worth raising with your bank if you plan to hold the loan for several more years.

What About Existing Loans? The Goodwill Discount

If you already have a car loan signed before 1 June 2026, it does not automatically convert to the new system.

But the banking industry has announced a “goodwill discount” initiative for existing fixed-rate hire purchase agreements settled early after the Act takes effect.

This is a voluntary early settlement rebate that banks will offer on outstanding interest for loans signed before the new law. It gives existing borrowers a more meaningful rebate than the Rule of 78 previously allowed.

What This Means If You Are Buying a New Car After June 2026

If you are taking a new car loan from 1 June 2026, three things are different from before.

First, you will see the EIR on your loan agreement and all marketing materials.

Use it to compare offers between banks rather than the flat rate.

Second, your interest is calculated on the reducing balance, meaning early settlement delivers real savings proportional to what you still owe. Third, you can sign your hire purchase agreement digitally.

The amendment also modernises the signing process to allow electronic and digital signatures.

One important note: during the transition period (June 2026 to March 2027), not all banks will have completed their system updates.

Some lenders may still be operating under the old structure during this window. When taking a new loan, ask your bank specifically which method they are using and request the EIR before signing. If they cannot provide it, that is a red flag worth taking seriously.