You have RM500. Maybe it is from your first month working. Maybe it has been sitting in a savings account earning 0.5% while you figure out what to do with it.

You know you should invest.

Every time you search for where to start, you end up in an article that assumed you already knew what an expense ratio is.

This is the version that starts from the beginning, uses real Malaysian examples, and answers the actual question:

What are ETFs, unit trusts and REITs, and which one do I start with when I have RM500 and no idea what I am doing?

The idea behind it

ETFs, unit trusts and REITs are all versions of the same core idea.

Most people cannot afford to buy a diversified portfolio of assets by themselves.

A 22-year-old with RM500 cannot buy shares in 30 different companies, cannot own a shopping mall, cannot invest across five countries. The money is too small to spread meaningfully.

All three solve that problem by pooling money. Thousands of investors each put in their small amount. The combined pool is large enough to buy a diversified set of assets.

Each investor owns a proportional slice. This is the shared logic underneath all three.

Once you understand it, the rest is just details about what kind of pool, how it is managed, how it is bought and sold, and what it costs.

ETFs: the low-cost version of a unit trust that trades like a stock

An ETF (Exchange-Traded Fund) is basically a unit trust that trades on the stock exchange, pooling money to invest in a basket of assets.

An index is a predefined list of companies based on specific criteria.

The FTSE Bursa Malaysia KLCI is an index of the 30 largest companies listed on Bursa Malaysia.

An ETF tracking the KLCI buys those 30 companies in the same proportions as the index.

It just owns everything in the index. This passive approach is why ETFs have much lower management fees than actively managed unit trusts.

Why the fee difference matters so much

A typical actively managed unit trust in Malaysia charges an annual management fee of 1.5 to 2%. A typical Bursa-listed ETF charges 0.4 to 0.7% annually. The difference between 1.75% and 0.5% sounds small.

Over 20 years, on RM500/month invested, that fee difference can result in a final portfolio value 15 to 25% lower for the higher-fee product, all else being equal. Fees add up against you just like returns add up for you.

This is the main reason why ETFs are better than actively managed unit trusts. Many financial advisors who make money by selling unit trusts don’t bring this up on their own.

What ETFs are available in Malaysia?

As of early 2026, there are 13 ETFs listed on Bursa Malaysia, covering Malaysian equities, ASEAN equities, US equities, Chinese equities, gold, and bonds.

Eight of the 13 are Shariah-compliant, screened by the Securities Commission’s Shariah Advisory Council. The minimum purchase is 100 units per lot.

Malaysian investors can also access global ETFs through international brokers or via locally available robo-advisors that build and manage global ETF portfolios automatically.

How to buy an ETF in Bursa?

- You need a CDS (Central Depository System) account and a stock trading account.

- You open both through a licensed stockbroker (most of which now offer a fully digital process taking 10 to 15 minutes).

- Once set up, you search for the ETF by its stock code, select the number of lots to buy (minimum 100 units per lot)

- Place the order.

- The process is identical to buying any stock on Bursa.

Unit trust: the one with the most hidden cost

A unit trust is a fund managed by a professional fund manager.

You put in money. The fund manager decides which stocks, bonds, or other assets to buy and sell.

You own units in the fund, and the value of those units rises and falls based on how the underlying investments perform.

You buy and sell through the fund company or their distributors, which in Malaysia typically means banks, financial advisors, or dedicated investment platforms.

How it works in practice

Imagine you put RM500 into an equity unit trust. The fund manager combines your money with thousands of other investors and buys shares in 80 to 150 companies.

Once a day, the value of your units is figured out by taking the total value of all the underlying shares and dividing it by the number of units that are out there.

This daily calculated value is the NAV (Net Asset Value) for each unit. NAV goes up when the companies in the fund do well, and it goes down when they do poorly.

You do not need a stock trading account to invest in a unit trust. You can invest through a bank counter, the fund company’s website, or online investment platforms.

Many unit trusts allow you to start with RM100 or even less per transaction. This low barrier is one of the genuine advantages for beginners.

The fee problem most people miss

Buying through a bank or agent usually means a 3–5% upfront fee. From your RM500, you lose RM15 to RM25 before your money has done anything.

Your investment effectively starts at RM475 to RM485.

On top of that, there’s an annual management fee of about 1.5–2%, charged regardless of performance.

If your fund returns 7% but you pay a 5% upfront fee and 1.5% annually, your first-year net return is only about 0.5%.

Over 10 to 20 years, high fees compound against you in a way that quietly costs far more than most investors realise.

ASNB & ASB : Malaysia’s most efficient unit trust

An important exception is ASNB (Amanah Saham Nasional Berhad) which manages ASB (Amanah Saham Bumiputera).

ASB has no sales charge or separate management fee and has delivered steady 5–7% dividends for decades, though it’s only for Bumiputera investors.

EPF members can also invest through i-Invest at a capped 0.5% sales charge per transaction, investing up to 30% of Account 1 savings above the Basic Savings quantum.

REITs: the simple breakdown

A REIT (Real Estate Investment Trust) is a company that owns income-generating properties like shopping malls, office buildings, hotels, hospitals, and warehouses. It is listed on Bursa Malaysia like a regular stock.

When the properties generate rental income, the REIT must by law distribute at least 90% of that income to unit holders as dividends.

This is the defining characteristic of a REIT and the reason they pay higher dividends than most other stocks.

Take Mid Valley Megamall for instance, which is owned by IGB REIT and has hundreds of tenants paying rent to IGB REIT. Most of that money is paid out as dividends.

So every time you spend there a small percentage goes to REIT investors. If you own units, that includes you.

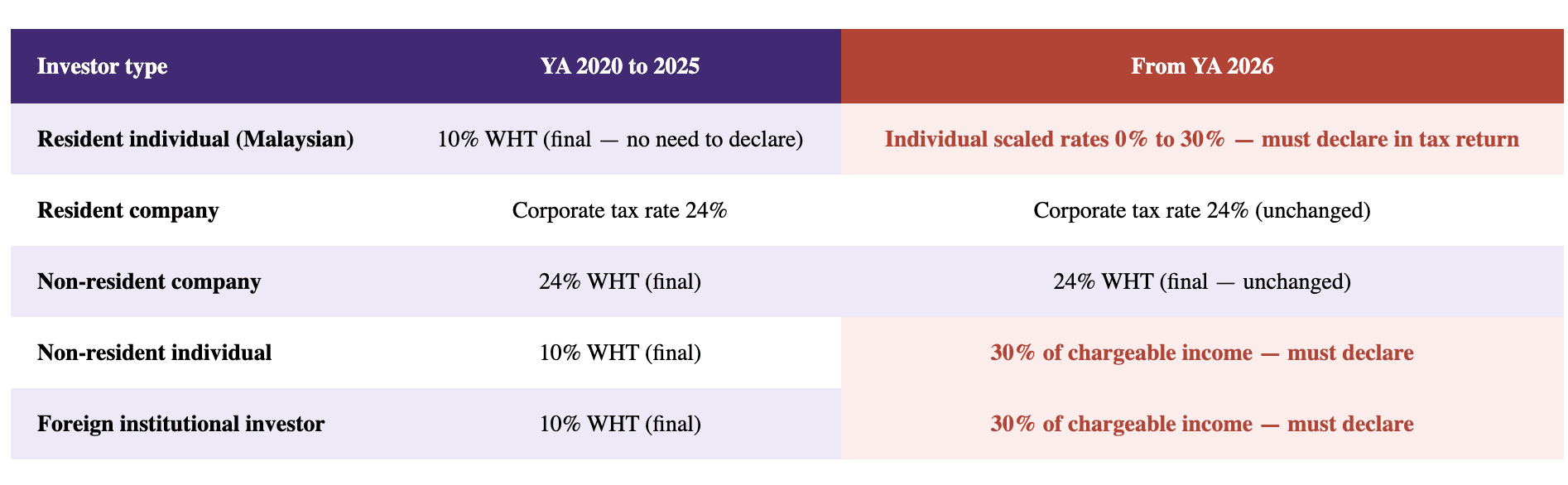

The 2026 tax change

LHDN Practice Note No. 2/2026 — Published 18 March 2026

The 10% preferential withholding tax (final tax) on REIT distributions that applied from 2020 to 2025 has been removed. From Year of Assessment 2026, Malaysian resident individual investors are no longer subject to withholding tax. REIT income must be declared in your annual income tax return and taxed at your personal scaled income tax rates (0% to 30%). You will need to report REIT distributions in your LHDN e-Filing from YA 2026 onwards.

What this means in real money for a Malaysian investor:

Under the old system, if you received RM10,000 in REIT distributions, RM1,000 was deducted as withholding tax and you received RM9,000 net.

No further tax declaration needed. The 10% was final.

From YA 2026, no withholding tax is deducted. You receive the full RM10,000.

However, you must now declare this as income in your annual tax return and pay tax on it at your personal income tax rate.

For most young Malaysians earning a modest salary, the scaled rate on REIT income may still be low. If your total chargeable income falls in the lower tax brackets, you might pay 1% to 13% on the REIT distributions rather than 10%.

If your total income is high enough to push you into the 25% to 30% bracket, the tax cost increases significantly compared to the old flat 10%.

Malaysian REITs and current yields

| REIT | Property type | Approx. yield | Notable assets |

|---|---|---|---|

| Sunway REIT | Diversified (retail, hospital, hotel) | ~4.88% | 20 properties across multiple sectors |

| KLCC REIT | Premium office and retail | ~4.0% | Petronas Twin Towers, Suria KLCC |

| Pavilion REIT | Retail focused | ~3.7% | Pavilion KL; RHB’s top 2026 pick |

| IGB REIT | Retail | ~3.1% | Mid Valley Megamall, The Gardens |

| CapitaLand Malaysia Trust | Retail and commercial | ~7.7% | 3 Damansara, Sungei Wang (FY2025) |

Side by side: how each one works

| Feature | Unit Trust | ETF | REIT |

|---|---|---|---|

| What it invests in | Stocks, bonds, or mixed. Fund manager decides. | Tracks an index passively | Income-generating properties |

| Minimum to start | From RM100/transaction | 100 units (RM70 to RM650) | 100 units (RM100 to RM2,000+) |

| Upfront sales charge | 0% (ASNB) to 5% (bank agent) | None (brokerage fee only) | None (brokerage fee only) |

| Annual management fee | 1.5% to 2.0%/yr | 0.4% to 0.7%/yr | Built into REIT operations |

| Regular income | Sometimes | Sometimes | Yes — 90%+ of rental income, quarterly/semi-annually |

| Tax on income (resident individual, from YA 2026) | Varies by fund structure | Capital gains generally not taxed (no CGT in Malaysia) | Scaled individual rates 0%–30%. Must declare in tax return. No more 10% WHT. |

| Need CDS/trading account | No | Yes (or robo-advisor) | Yes |

| Shariah-compliant options | Yes, widely available | Yes, 8 of 13 Bursa ETFs | Yes, 4 i-REITs (KLCC, AXREIT, others) |

The fee difference over time: why it matters more than it looks

Imagine you invest RM500 per month for 20 years. The underlying investments perform identically at 7% annual return in all scenarios. The only difference is fees.

| Scenario | Fees assumed | Final value (20 yr) | vs High-Fee |

|---|---|---|---|

| Unit trust via bank agent (5% sales + 1.75%/yr) | 5% upfront + 1.75%/yr | ~RM196,000 | Baseline |

| Unit trust via platform (0% sales + 1.5%/yr) | 0% + 1.5%/yr | ~RM222,000 | +RM26,000 |

| ETF or robo-advisor (0.5% all-in) | 0% + 0.5%/yr | ~RM275,000 | +RM79,000 |

The RM79,000 difference between the low-fee ETF scenario and the high-fee bank unit trust comes entirely from fees.

The underlying investment generated the same returns. The only difference is how much was taken out along the way.

That RM79,000 is roughly 31 months of salary at RM2,500/month, compounding away silently without you ever writing a cheque or seeing it leave your account.

This is why financial literacy about fees matters more than most people realise at the beginning.

With RM500, where do you actually start?

Three options, three different purposes

ETFs, REITs and unit trusts are not competitors. They serve different purposes and in the long run most investors will use a mix.

ETFs/robo-advisors are the long-term growth engine, low cost, diversified and built for compounding with less effort.

REITs are the income engine, dishing out regular dividends and giving exposure to real estate without owning the property.

Unit trusts serve to actively managed funds with specialist mandates, and a seamless monthly investment flow that requires no stock trading knowledge.

ASNB funds in particular, for eligible Malaysians, represent a return profile that no ETF or REIT consistently matches on a risk-adjusted basis.

Same goal, different tools.

The checklist

- 1Emergency fund first. 3 to 6 months of essential expenses in a liquid account before you invest RM1 anywhere.

- 2Know all the fees before you commit. For unit trusts: sales charge plus annual management fee. For ETFs and REITs: brokerage fee including minimum charge. For platforms: check for additional platform fees on top.

- 3For REITs from YA 2026: understand your tax obligation. REIT distributions must be declared in your annual income tax return. No more final 10% withholding tax. Your effective rate depends on your total chargeable income. If you are in a low income bracket, this may be neutral or beneficial. If you are a higher earner, factor the higher tax cost into your yield calculation.

- 4Match your investment to your timeframe. Money you need in one to two years should not be in equities or REITs. Markets can lose 30 to 40% in a bad year and take years to recover.