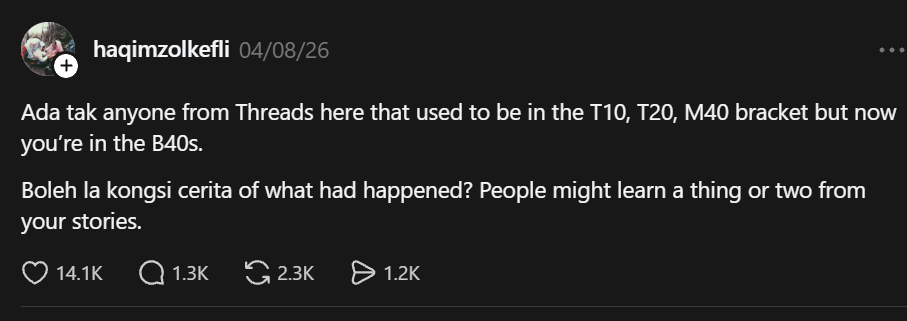

Recently, a single Threads post has gotten many Malaysians reflecting on their own lifestyles, income choices, and how stable their finances really are if disaster were to suddenly strike.

Posted by user @haqimzolkefli, the question was simple but hit different:

Is there anyone here who used to be in the T10, T20, or M40 bracket but is now living as B40? Feel free to share your story and what happened. People might learn a thing or two from your experiences.”

And learn they did. The post pulled in over 14,100 likes, 1,300 comments, and 2,300 reposts. The replies that came flooding in were raw, honest, and sometimes gut-wrenching.

Because as it turns out, the fear of losing your financial footing is something almost every Malaysian carries quietly. This post just gave them a safe space to say it out loud. The comments section quickly became a support group nobody signed up for but everyone needed.

From luxury lifestyle to starting over

One netizen, who claimed his family was once part of Malaysia’s top 1%, shared that his father was once the Director of Nokia Malaysia and even personally presented the first Nokia phones to Tun Mahathir.

Their family reportedly owned a house near Hyde Park in London, properties in Australia, and several homes across Malaysia. But after Nokia collapsed, bad investments started piling up, Microsoft acquired the company, and the family’s financial situation slowly crumbled.

Although the income stopped coming in, the spending habits remained the same, and within 10 years, everything was gone. Now 30 years old, the netizen said he is rebuilding his life from scratch with a simple mindset: “Slowly keep moving forward.”

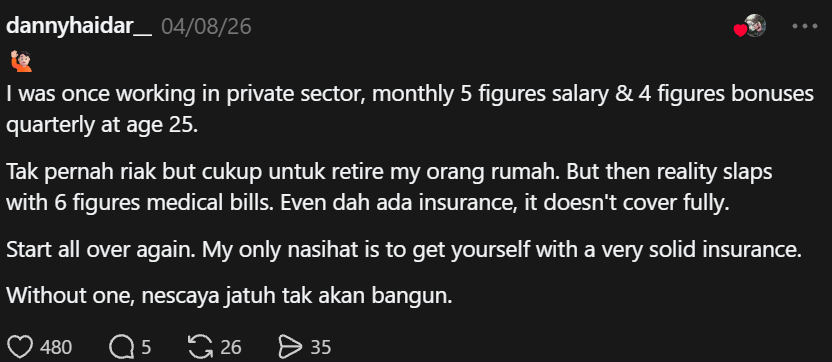

A medical bill changed everything

Another netizen revealed that he was earning a five-figure monthly salary at just 25 years old, complete with four-figure quarterly bonuses and enough money to retire his parents.

However, things changed after a family member was hit with a six-figure medical bill. Despite having insurance, it was still not enough to fully cover the costs, forcing him to start over financially.

He advised others to invest in proper insurance coverage, saying without it, “If you fall, you may never recover again.”

Hit by Covid

And perhaps the most heartbreaking reply of all came with no username attached:

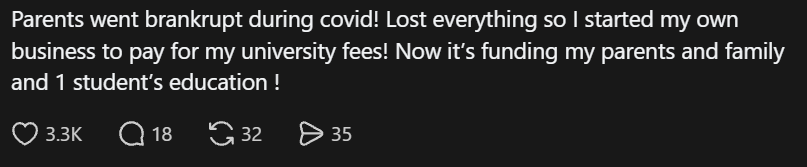

Parents went bankrupt during Covid. Lost everything.”

That person started a business just to pay for their own university fees. Now that same business funds their parents, their family, and even a student’s education. No pity party, just pure grind.

The reasons for falling were all different. Retrenchment. Medical emergencies. A trusted friend turning out to be anything but. A global corporate collapse. A pandemic wiping out a family’s entire financial foundation.

But the thread that connected all these stories was the same: it rarely took more than one thing to unravel years of hard work.

The statistic back it up

Here is the thing, these are not isolated horror stories. They are statistically documented and more common than most people are comfortable admitting.

According to stats from DOSM, when Covid-19 hit, Malaysia’s income landscape shifted almost overnight. According to DOSM’s Household Income Estimates and Incidence of Poverty Report 2020, a whopping 12.8% of T20 households dropped into the M40 group, while 20% of M40 households, around 580,000 families, slipped into B40 territory.

That is more than half a million families who went to sleep in one income bracket and woke up in another.

Many middle and upper-middle income households may appear financially stable on the surface, but heavy commitments such as housing loans, car loans, and other long-term debts can quietly place them under significant pressure. In situations where unexpected crises like medical emergencies, job losses, or business failures happen, even families with relatively high incomes can struggle to cope.

There is also a bigger structural problem hiding in plain sight. The T20 threshold starts at around RM10,960 per month, which might feel comfortable in smaller towns but is barely enough to breathe easy in Kuala Lumpur or Johor Bahru.

Being labeled T20 does not automatically mean you are financially secure. It just means you earn more than 80% of the country on paper.

Critics and researchers have long pointed out that the classification does not factor in household size, number of dependents, locality, or the rising cost of urban living, which means a lot of “T20” families were always more fragile than their bracket suggested.

The Bracket Is Not the Person

What the Threads post and all its replies really showed is something that Malaysians have known quietly for a long time: income brackets are not identities.

They are just snapshots. And snapshots change.

The Nokia director’s son lost properties across three countries and is now, at 30, slowly rowing back. The guy who got cheated by a friend turned that humiliation into a RM2 million company. The student whose parents went bankrupt is now funding another person’s education.

Falling is common. Falling is documented. But falling does not have to be the final word.

What separates a setback from a full collapse is preparation, solid insurance coverage, manageable debt, an emergency fund, and the mental resilience to get back up when life decides to rearrange your financial situation without warning.

No bracket lasts forever. Not the bottom, and not the top. Stay vigilant, stay adaptable, and when it happens, because for many of us it will, be ready to kayuh balik.