Buying your first home is a huge milestone for many people.

After going through the long process of paying the booking fee, securing loan approval, and signing the Sale and Purchase Agreement (S&P), most buyers feel relieved thinking the hardest part is already over.

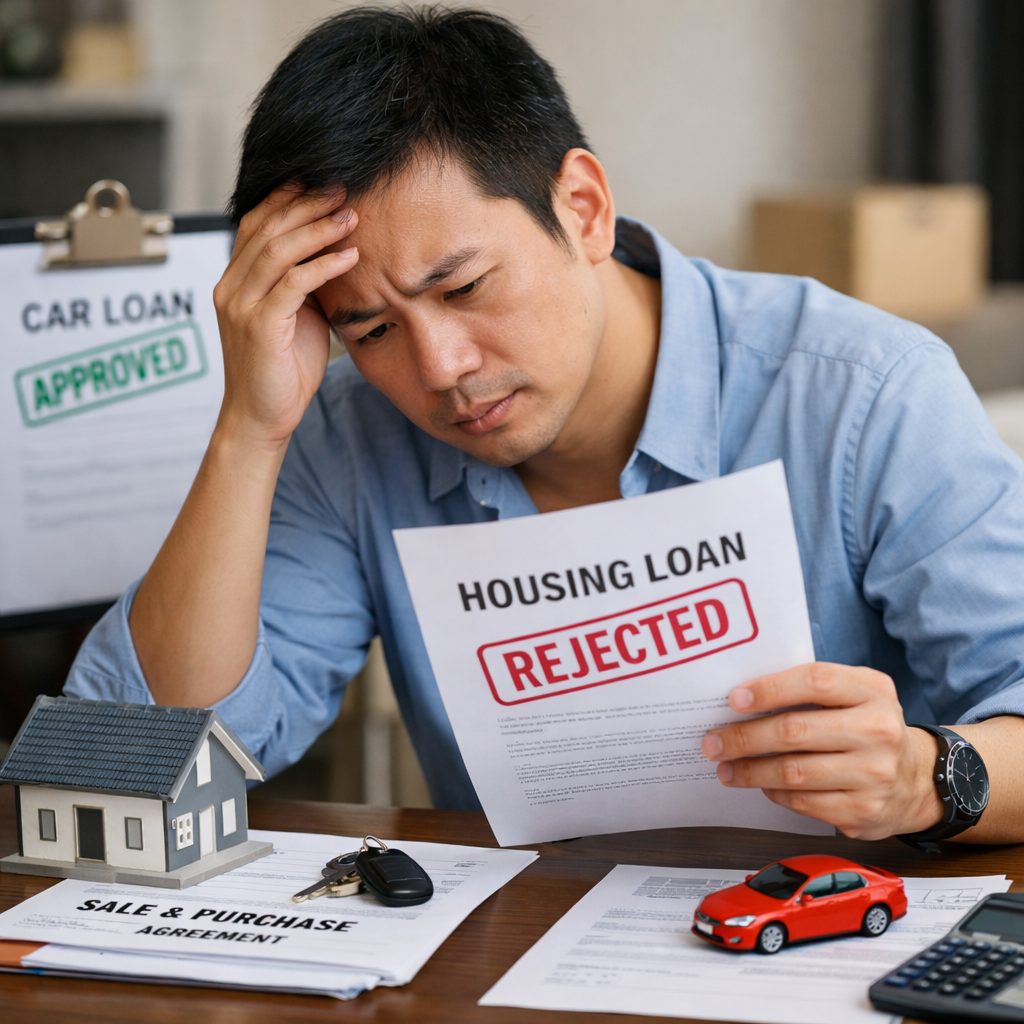

However, a Malaysian property advisor recently warned that some first-time buyers still end up losing their housing loan approval at the final stage due to a mistake they didn’t realise could happen.

Some buyers ‘tersungkur’ right before getting the house

In a video shared online, property advisor @agent_iskandar.property explained that it is not uncommon for buyers to stumble right at the finishing line.

“Your housing loan is approved. You’ve paid the booking fee and signed the S&P. You feel extremely relieved, right?

“But many first-time homebuyers end up falling at the last step because they do one thing before receiving their house keys,” he said.

The mistake many buyers make after their loan gets approved

According to him, the problem usually starts when buyers assume everything is settled once their housing loan has been approved.

Feeling excited about their upcoming home, some buyers immediately start taking on new financial commitments.

A common example is heading straight to a car showroom.

Since the house loan is already approved, some people think it’s the perfect time to upgrade their car too,” he said.

But this move can actually backfire.

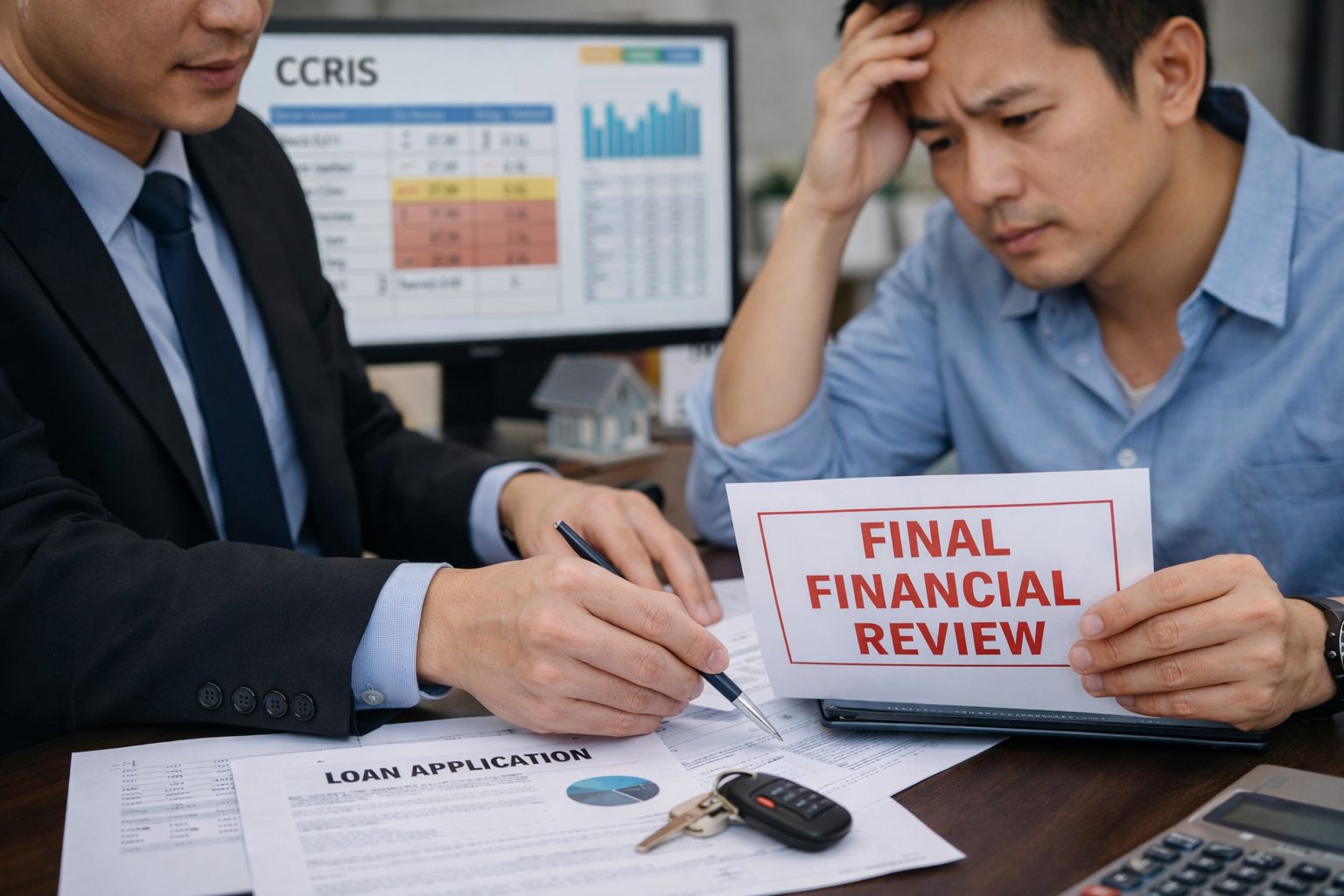

Banks still perform a final financial check

Many buyers are unaware that banks will still conduct a final financial review before releasing payment to the property developer.

During this stage, the bank may check the borrower’s latest financial status through systems such as CCRIS.

If new debts appear in the system, the bank has the right to withdraw the housing loan approval immediately.

This can happen even if the buyer has already:

- Paid the booking fee

- Signed the Sale and Purchase Agreement (S&P)

- Received earlier loan approval from the bank

Why taking new loans can cause your housing loan to be cancelled

The main reason is because new financial commitments can affect the borrower’s Debt Service Ratio (DSR).

DSR is the ratio banks use to determine whether someone can afford their monthly loan repayments.

When buyers suddenly take on additional loans, their DSR may increase beyond the bank’s approved limit.

This means the borrower may no longer qualify for the housing loan even though it was approved earlier.

Imagine you’ve already paid the deposit and signed the S&P, but the house slips away because your DSR ‘pecah’ after taking a new car loan,” he explained.

Things first-time homebuyers should avoid before getting their keys

To avoid such situations, the advisor urged buyers to avoid making any new financial commitments until the house keys are officially in their hands.

Among the things buyers should avoid are:

- Taking new loans such as car loans or personal loans

- Becoming a guarantor for someone else’s loan

- Maxing out credit cards or significantly increasing spending

Wait until the keys are in your hands

While buying a home is exciting, the process is not truly complete until the bank releases payment and the keys are handed over.

Taking on additional commitments too early could put the entire purchase at risk.

For many first-time homebuyers, waiting just a little longer before making big financial decisions could mean the difference between finally owning their dream home or losing it at the very last moment.