Many people believe that making smart financial decisions will always lead to long-term benefits.

Whether it’s buying property, investing in stocks, or starting a side hustle, the expectation is that these choices will eventually pay off.

But what happens when an investment doesn’t turn out as expected? Instead of generating profit, it becomes a financial burden, one that lingers for years.

This was the reality for one Malaysian homeowner who shared their frustrating experience of buying a house, only to regret the decision six years later.

A decision that felt right at the time

Like many others, they had high hopes when purchasing their home. The location seemed perfect; not too far from work, making daily commutes easier. It felt like a smart, practical decision.

But as time went on, things didn’t go as planned.

Development in the area picked up, and with it came something every driver dreads; endless traffic jams. What was once a convenient location turned into a daily headache, with hours wasted on the road.

Life throws a curveball

Just as they were trying to deal with the worsening traffic, life took an unexpected turn. Their husband got transferred to a state on the East Coast, forcing them to make a tough decision; stay behind or move together.

In the end, they chose to relocate.

That meant leaving behind the house they had spent so much on. And with no one living there, renting it out seemed like the best option.

Renting it out, but still feeling the pinch

At first, it seemed like things would work out. They managed to find a tenant willing to pay RM1,000 a month. But there was a catch, their monthly loan repayment was RM1,700.

We rent it out for RM1,000, but we still have to top up RM700 every month. It doesn’t feel like an investment. Every time I have to make the payment, I get annoyed,” they admitted.

While RM700 a month might not seem like much at first, the numbers add up over time.

Over RM50,000 lost in loan top-ups

Since they had been topping up RM700 every month for six years, here’s how much they actually lost:

RM700×12 months×6 years=RM50,400

That’s over RM50K spent on loan repayments for a house they neither lived in nor wanted to return to.

No wonder they started to regret their decision.

6 years later, the regret still lingers

With six years of loan payments behind them, the homeowner still struggles to accept the decision they made.

Every day, I wonder if there’s a silver lining to this. Imagine, RM1,700 could have been savings… wouldn’t that have been a happier choice?” they reflected.

Now, tired of being stuck in this financial mess, they have decided to sell the townhouse and move on.

Others offer advice on how to handle the situation

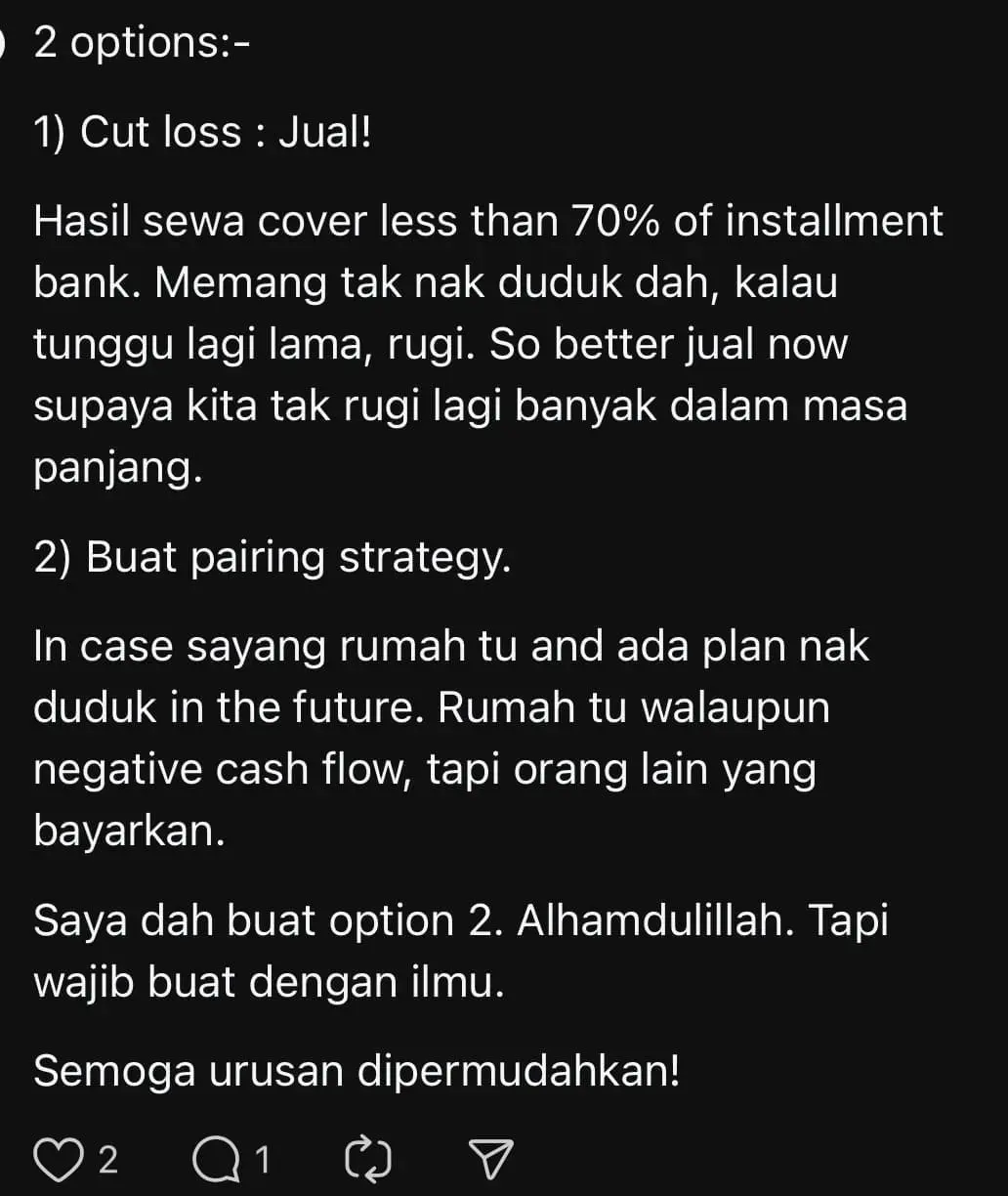

While many could relate to the homeowner’s struggle, some netizens offered practical advice on what they could do next. One person outlined two possible options:

“You have two choices:

- Cut your losses, sell the house. Your rental income covers less than 70% of the bank loan. Since you don’t plan on living there anymore, the longer you wait, the more you’ll lose. It’s better to sell now before the losses pile up.

- Use a pairing strategy. If you still have sentimental value for the house and plan to live in it one day, let your tenants continue paying for it. Even if the cash flow is negative, someone else is helping with the loan.

I personally went with the second option, and Alhamdulillah, it worked out. But you must do it with proper knowledge. Hope everything works out for you!”

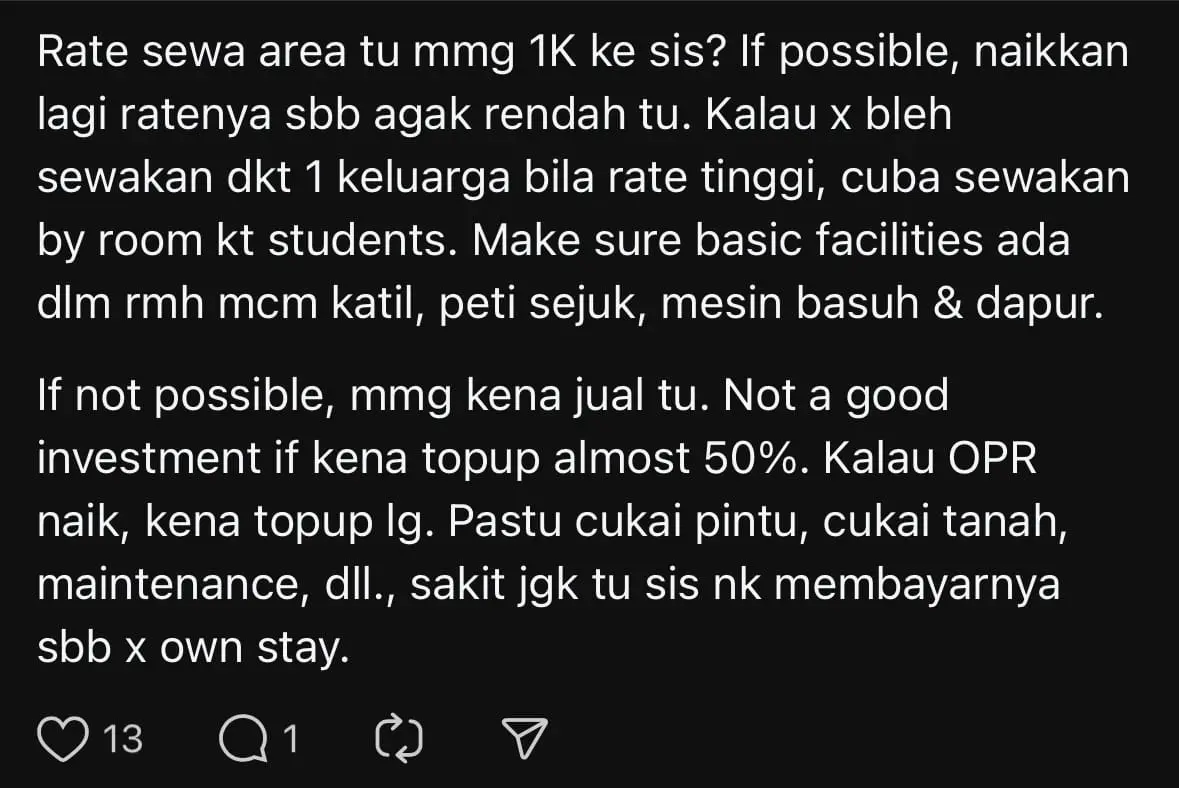

Another netizen questioned whether the rental rate was too low and suggested ways to maximize returns:

“Is RM1,000 really the average rental rate for that area? If possible, try raising it because that seems a bit low. If a single family isn’t willing to pay more, consider renting by room to students instead. Just make sure the house has basic necessities like beds, a fridge, a washing machine, and a kitchen.

If increasing rent isn’t an option, then selling might be the best move. It’s not a good investment if you’re topping up almost 50% of the loan every month. And if the OPR (Overnight Policy Rate) increases, you’ll have to pay even more. Plus, there are additional costs like property taxes, land tax, maintenance fees, etc. It’s a financial strain if you’re not even living there.”

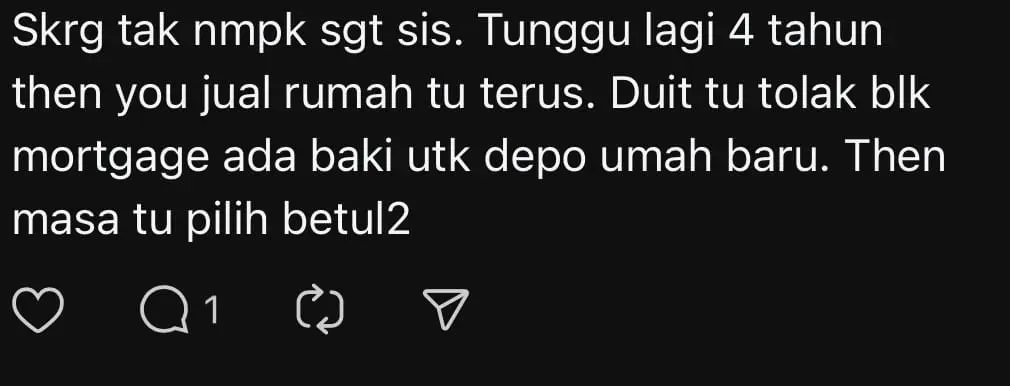

One user suggested holding onto the house a little longer before making a move:

“You might not see it now, but wait another four years, then sell the house. By then, you can use the remaining balance from the sale after settling the mortgage as a deposit for a new home. Just make sure to pick wisely next time.”

Read the original post here:

View on Threads